Stock Market Corrects-Covid Disrupts Economy

Whilst the stock market may be moving into correction territory, we look to the past to learn more about what may happen within the next year to ten years.

I missed last weeks blog due to exactly what the title says above, Covid doesn’t disrupt the economy, it disrupts lives!

I have been sitting in bed the last three to four days with what has felt like the worst flu of my life, nausea, dizziness, constant headaches, lack of any energy at all and to top it off, my nose just started running…

But we aren’t here to take pity on my plight, if anything we are here to take in the lessons of the last two years. And one thing we have learnt from the last two years is that the economy is set-up by human productivity, and Monetary policy.

So what happens when monetary policy (money-printing from the central banks) will start to ease by potentially as early as the end of next month due to the most recent CPI (Consumer Price Index) report?

**If you are unsure of what the CPI report is and inflation in general, check out this website https://www.investopedia.com/terms/i/inflation.asp

What happens when schools go back and we potentially get an up-tick of Covid cases and therefore more people isolating at home? Therefore decreasing productivity…

I am not one to make predictions or bring out the crystal ball, however I can definitely see how the economy may slow down a little this year, or at the very least within the short-term.

You can see this portrayed through the volatility we have seen in the stock market recently!

All you have to do is check out the last week in the ASX200…

The ASX 200 over the last 5 Trading Days is down 6%

Which is moving into correction territory, which is when we see a drop of 10%.

Source: google.com.au/ASX 200 chart

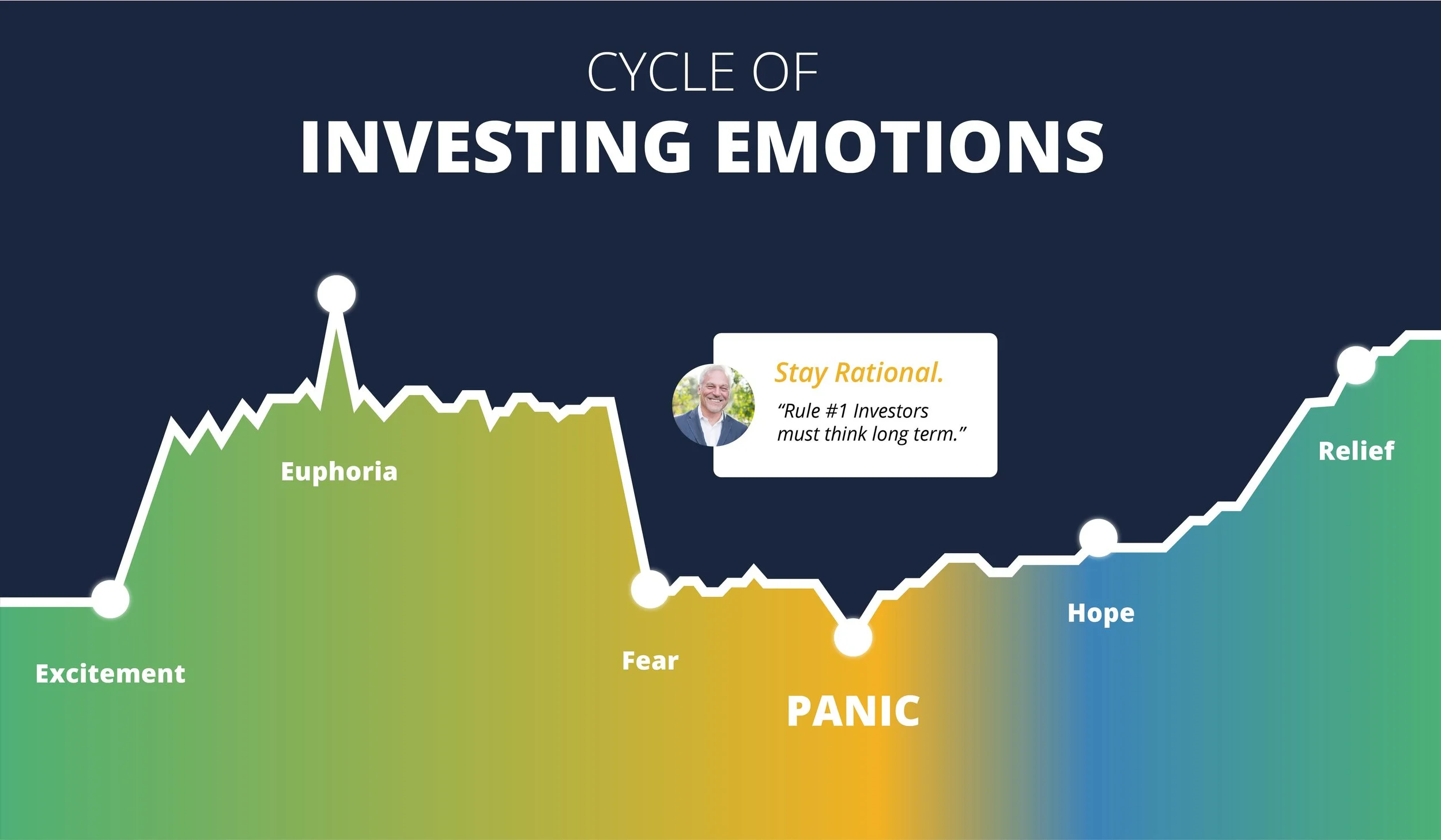

I am not trying to bring out a fear at all about the market dropping or the economy slowing, but I do want to bring you the facts, just as Covid has disrupted our lives for the last two, nearly three years, there will be more disruptions to come.

You need to know the facts, to make educated decisions and understand that this year may be a tough year for investing.

But there is a silver lining!!

Where there are corrections and down times in the markets, this brings about opportunities for us investors.

I want to teach you the most important lesson as an investor in the equity markets, by simply showing you the graph below;

What you see above is 100 years of data from the All ordinaries index, which later was taken over by the ASX 200 inde. Now as you can see, there are a heap of downturns and corrections in the market, but the main thing I want you to concern yourself with is the starting point of the graph on the y-axis at the very left of the image.

You can roughly see that at the year 1900, the index was priced at about $50, by the end of the century we can see that the markets had increased significantly, even with a heap of downturns and multiple years of catching back up afterwards. The market always ends up better off.

That is why you should not concern yourself with the recent drop in the market, nor the disruptions happening with Covid still running rampant within the community.

If history is anything to go by, we will see the market back in the green and making leaps and bounds, when that will happen, we do not know, but right now, when the market is fearful, it is the best time to invest!

In my next blog, I will be completing the beginning investor series, I look forward to seeing you then,

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

________________________

** The article above only should be used for educational purposes only and is not financial advice, if you wish to invest in the equities market, I highly suggest that you seek advice from a professional that you trust!

The Ultimate Investing question… Passive or Active?

The age old question you need to answer for yourself before you start investing is whether you will be an active investor or passive…

For the majority of you, it will most likely be the latter, but read my blog on the advantages and disadvantages of both.

Investing is really important to growing your wealth and getting to the point where you do not have to work, rather you can choose to work.

Therefore, this is a must read!

Over millennia, we have seen debates around the world about whether you should be an active investor, whereby you have a pretty active role in choosing the assets you buy and sell in your portfolio. Or whether to be a passive investor, whereby you follow the market or a trend you believe will be big in the future.

Over the course of the last few decades, we have seen a pivotal change in the overall consensus of investing, with more people moving into the passive camp.

Today, I want to highlight the advantages and disadvantages of both and to educate you on why I have decided that I shall be an active investor for my own portfolio.

Once you have read through it all, it is up to you to make up your own mind about what style of investor you are going to be.

Passive Investing: “Passive investing is an investment strategy to maximize returns by minimizing buying and selling. Index investing in one common passive investing strategy whereby investors purchase a representative benchmark, such as the S&P 500 index, and hold it over a long time horizon.” - [1]

Advantages:

Diversification, being able spread risk broadly, such as when you invest in the broader market, such as an S&P 500 index.

Lower fees

Tax efficiency

Less time needed for research, simplicity: You do not need to research into every stock or financial product.

Can dollar cost average, instead of timing the market: You can decide to invest a small sum of money every month, three months etc. Rather than trying to time the market, you consistently invest for a set period of time.

Disadvantages:

Subject to total market risk: Whereby if the broader economy is not doing so good, the markets will correct/crash.

You will not see returns higher than the market: As most passive funds, ETF’s etc. They only track the overall market performance.

Seems like a pretty good idea, rather than doing all the work to research the market, just follow the overall market trajectory and returns. You spend less on fees and it is much more tax efficient to put all your money into one index. In fact, for 80-90% of you who are reading this blog right now, it is probably the most effective way to start and continue investing for the long term.

However, with the current market climate and with interest rates on the expected rise, I suspect that active investing will get bigger again over the next few years…

Let’s see why!

Active Investing: “Active investing refers to an investment strategy that involves ongoing buying and selling activity by the investor. Active investors purchase investments and continuously monitor their activity to exploit profitable conditions.” [2]

Advantages:

Flexibility: Active managers aren't required to follow a specific index. They can buy those "diamond in the rough" stocks they believe they've found.

Hedging: Active managers can also hedge their bets using various techniques such as short sales or put options, and they're able to exit specific stocks or sectors when the risks become too big. Passive managers are stuck with the stocks that the index they track holds, regardless of how they are doing.

Tax management: Even though this strategy could trigger a capital gains tax, advisors can tailor tax management strategies to individual investors, such as by selling investments that are losing money to offset the taxes on the big winners.

Risk management: Active investors and fund managers can select stocks based on the prevailing market conditions.

Short-term opportunities: Active investors can make use of short term (3 months or less) opportunities, which in turn gives them a range of tools to choose from when investing.

Have more opportunities to invest in different asset classes: Active investors and funds are more likely to be able to delve into different asset classes, therefore diversifying risk away again.

Can meet specific needs of ethical and moral criteria: With most passive funds, a lot of them do not meet a lot of investors criteria, such as not to invest in mining, or child slavery. When you invest in the top 500 companies in the U.S for example, you have no idea what these companies are doing with your money.

Disadvantages:

Very expensive: The average expense ratio is 1.4 percent for an actively managed equity fund, compared to only 0.6 percent for the average passive equity fund. Fees are higher because all that active buying and selling triggers transaction costs.. All those fees over decades of investing can kill returns.

Active risk: Active managers are free to buy any investment they think would bring high returns, which is great when the analysts are right but terrible when they're wrong.

Poor track record: The data show that very few actively managed portfolios beat their passive benchmarks, especially after taxes and fees are accounted for. Indeed, over medium to long time frames, only a small handful of actively managed mutual funds surpass their benchmark index.

Minimum Investment amounts: Some Actively managed funds in fact need a minimum to invest in that fund, such as $10,000. Or some brokerage platforms need a minimum of $100 per trade etc.

As you can see, the age old question of Active versus passive comes down to a few things, whether you have the time to do the research, whether you are ok taking on more risk for more specific investments, and also whether you can take on some more complexity regarding tax etc.

At the end of it all, it mostly comes down to whether you also believe the wider market will do well over the long term or whether you have the confidence and knowledge to beat the markets over the long term.

Majority of the time, you won’t beat the market, so it is truly up to you to decide whether you are a passive or active investor.

I have decided that I want to follow along the path of active investing, to test my own knowledge and because I believe that the overall markets will not increase significantly over the next ten years. I do not see a lot of growth to be had, however I may be entirely wrong and therefore you need to make your own decision on what you should do as an investor.

Let me know in the comments below what path you will choose,

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

_______________________________________

References List:

[1] - https://www.investopedia.com/terms/p/passiveinvesting.asp

[2] - https://www.investopedia.com/terms/a/activeinvesting.asp

New Year brings New Achievements!

One of the most important parts of the process to Taking Back Control your Life-Health-Wealth is to start setting goals.

Joel Perryman runs through how he sets his own goals with his wife and gives you a quick example of one of their dreams!

Every year I will sit down and reflect, however, that is only one part of the process that has helped me to Take Back Control of my life, business, finances, relationships and health.

On Monday, my wife and I sat down to plan out our goals for 2022, which is an integral part of being able to Take Back Control.

The first phase of understanding what you want to achieve is understanding where you are right now and knowing what your dreams are.

There was a phrase I learnt from the great Tony Robbins that is a four step process used to creating achievements and it went like “Dream-Goal-Plan-Action.”

You have to be able to have a dream and vision for what your future will be like, then you must write that down to become a goal and set a timeline for it, create a step-by-step plan to achieve it and then take action on the plan. Seems pretty simple and it really is, although there is one more step that needs to be added to the process which becomes pretty important from my experience…

That step is being able to reflect on where you have been, what you have achieved and what you have learnt, adding the reflection process in with Tony Robbin’s four steps to achievement process is much more effective and is quite similar to the SMART-ER goal principles for creating goals.

SMARTER goals means “Specific-Measurable-Achievable-Relative-Timely-Evaluate and Re-assess.”

Now, you don’t need to know all of the theory, but understanding that this stuff truly works and is really simple to follow is imperative to creating success, taking back control and achieving more from life.

On Monday, when my wife and I sat down to map out our year for 2022, we utilised the processes above in a very simple way.

We sit down and jot down the main categories that we need to grow in each year to feel fulfilment and purpose in life, you don’t need to just do these five, you could add more if you like, but here they are;

Relationships

Health

Education

Career/Business

Finances

Under each of them, my wife and I will talk about what we want to achieve in each of these main areas in our lives for the year and write down our goals and when to achieve them by. However, my wife and I have discussed at length what we want to achieve together and know pretty well where we want to take our lives.

Becoming clear on what your lifestyle will look like together in 5, 10 even 20 years from now is just as important to creating your goals. Which is probably a conversation you should have with your partner, or having a conversation with a friend if you are single, to get a bit more clear on what your lifestyle and dream for your life will look like. (If you need help on getting clear on what your life will look like, have a read of one of my first few blogs here )

Your dream/aim for your lifestyle does not have to be exact, it just has to be a vision of what it may look like and that is when you can start breaking down how to achieve your dreams.

My wife and I do this through reverse engineering, or essentially taking backwards steps from the dream. Let me take you through a quick example of one of our goals.

We want to move into our dream family home, as one of our goals is to start creating a family of our own. The goal required extensive research, financial planning and much more. Thankfully, I am studying to be a financial planner and a mortgage broker, which made that side of things a whole heap easier, and we have also bought a house before as well.

Ps. With experience and knowledge we have been able to make quick and calculated decisions through planning and taking action, that is why you should seek advice from a professional and leverage their knowledge to make the goal seem attainable. Which has led us to be able to make quick decisions like we did for when we bought land and found a builder for our dream home to be built by mid-2023.

First and foremost, we have a dream of creating a family and having a four bedroom home for that family. Once we have the dream, we set a goal pertaining to achieving the dream, which for us was a few different goals under different categories.

Under relationships, my wife and I placed “Start trying to have a baby by December,” under Finances we placed “sell house” and “save $20,000 by end of year.”

Under career/business, my wife decided her main goal was to “remain consistent in her job,” and for myself it was to “start working as an associate planner part-time once we sell the house.”

As you can see, once you have been able to create your dream, the goals are just stepping stones towards it, the goals become your plan and all you need to do is take ACTION on that plan/goals.

Goal setting is imperative to Taking Back Control of your Life-Health-Wealth and using the start of the year to evaluate and adjust goals as needed is an important part of that process.

You could even evaluate your goals every six months, or even every three months. The last two years have shown just how quickly things can change, which means your goals may need to change along with the world as well.

To summarise on how to start writing down your goals you need to;

Get clear on your dream/lifestyle for the next 5, 10 or 20 years

Reverse engineer how to achieve your dream (Ask a professional or someone who has done it before, they can help here.)

Write down your stepping stones (goals/plan) and make them SMART-ER.

Once you have the goals and your plan, purely and simply take Bold Action!

Use the above to help you get clear and if you need any more help, write a comment below and I would love to get back to you on how you can truly Take Back Control.

Until next time, where I will be getting back to the beginner investor series for the last two blogs!

See you then,

TBC

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

That’s a Wrap… 25 Wins for 2021!

Winning at life comes down to perspective, everyone always has some wins from the year if you can sit down and actually start thinking about what wins you had for the year!

You can find wins in health, investing, personal finances, wealth, relationships and wins.

With only two more days left of 2021, I have been sitting back and reflecting on the year that was. From my reflections I have come up with the best way to describe the year 2021, a ROLLERCOASTER of EMOTIONS!

With so many highs and so many lows on a personal level, from getting married, to deaths in the family and amongst friends, to lockdowns and business closing/re-opening…

The year has provided myself with many lessons and teachings, however even with so many lows, I have also had a heap of highs…

Every year I go through the top 25 wins for the year on a personal level and even with a tumultuous year like 2021, I was still able to find 25 wins to share with you today, so here it goes…

Getting Married to Liv (In the middle of a pandemic)

Bringing Marlow into the Family (Our golden retriever puppy)

Thriving through 2021/lockdowns

Buying land in Officer for our dream house (in lockdown)

I got clear on my career path and got clear of what Liv and I want.

Decided on a builder for our dream home

Having a mini get-away and booking our honeymoon to QLD (2022)

Being truly open with Liv and getting closer in our relationship throughout the lockdown.

Re-opening UFT after closing it for the sixth time

Got back into running 1-2 times per week

Completed a full time load of Uni

Completing the Business Career Mentoring Program with my mentor, Tom

Improved my network and connections with people that could help me achieve my own path forward

UFT got back to pre-lockdown levels

Was able to maintain healthy habits through a our sixth lockdown

Built my portfolio from $7k to $15k

Feeling closer to family than I have ever been before

Sold my car and brought a second hand car to last the next 12-18 months

Started researching relentlessly on Web3.0 and crypto/investing

Gilbert Graduated as a Seeing Eye Dog

Making some big changes to UFT (To come mid Feb)

Launched this blog, Take Back Control, to help people improve their life-health-wealth.

Became more aware of my own superpowers (strengths- Practical optimism, Positivity, Organisation, Research/reading, writing, goal-setting) and Kryptonite (weaknesses- Kind Candour, Giving feedback, completing jobs fully due to having too many, procrastinating due to overloading on work)

Letting go of resentments and understanding my own emotional intelligence better

Finding a balance and understanding how to switch hats when needed

The year 2021 has been a profound year for most, I am sure of it, we have all started to understand the importance of the environment we surround ourselves with. Which has led to a lot of personal revelations for a lot of people, which is why I believe that 2022 is going to be an amazing year.

The year is going to be busy and fly by, but I know that 2022 is going to be huge!!

My next blog will be on my goals for 2022 and how to actually you can set goals for yourself as well, in the meantime, I would love to hear your wins for the year. You may not do 25, but even if you aim for 10, the main thing is to sit down and reflect on your year.

You can use this time of reflection to understand more about yourself and even help you to shape your 2022!

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

What are the differences between ETF’s and Managed Funds?

The age old question of investing, do I invest passively or actively?

Do I entrust my money to a professional or believe in the overall market/economy?

Joel Perryman delves into what an ETF and a Mutual Fund is and goes through a little bit about active v. passive investing.

A lot of people that start investing just put there money into something their friends have said has been working really well for them. You probably have heard of particular stocks that have been doing well or maybe delved into some crypto…

Unfortunately, by doing this, you are taking a punt, without actually understanding the underlying fundamentals of the stock or crypto, you are essentially better off picking a horse at the Melbourne Cup because you like the look of it and its name is really cool.

Which is why I wanted to delve into this investing series in the first place, to give you, a beginner to intermediate investor, an understanding of how to use your money to grow your wealth and to not flush it down the drown on a few bets you took on a business or coin that your friend suggested.

What has that got to do with understanding what ETF’s and Managed funds are?

Well, quite a lot, because again, people are just putting money into these “safe-havens” without truly understanding what they are.

You should know where you are putting you money and understand exactly what is happening with it, that way you can sleep well at night knowing the your money is being used for good and also that you won’t lose half of it literally overnight.

Let’s delve into what I think an Exchange Traded Fund and Managed Fund is…

An ETF is a basket of stocks, commodities, real-estate and even crypto these days that can be exchanged on a local stock exchange, such as the ASX (Australian Stock Exchange).

Essentially, it can track an index, which is a method to track the performance of a group assets in a particular market, eg; the ASX 200 which tracks the performance of the top 200 companies within Australia. (1)

Whereas a Managed Fund (or Mutual Fund for the proper term) is where a large number of investors pool there money and entrust a particular fund/investor to invest on their behalf. (2)

Which means that you could gather 10 friends and all put $2,000 into a trust/account and entrust your investor friend to use your money and invest it into particular stocks, commodities, REIT’s etc. Expecting that your investor friend can beat the market average over time.

Now you know the difference between the two, which is the best investment vehicle for you?

And that comes back to the question of the last ten to twenty years…

Do you invest Passively or Actively?

ETF’s are generally quite passive in nature, as they will just follow the broader market, where as a Mutual Fund is generally quite active, as they have someone choosing which stocks, ETF’s or assets to invest in.

Passive investing normally has less costs involved and is more of a set and forget approach, although I never would suggest just forgetting about where you have invested your money. For most people, this method of investing will work and work quite well in fact.

As you are investing in the broader market, through an ETF, you will have diversified your portfolio significantly, reducing risk overall.

And you just put small chunks of money in over time to grow your passive portfolio, meaning you don’t have to spend huge amounts of time researching individual companies or the markets.

However, it does not mean there is no risk involved, as there is an overall market risk if that particular index falls by 20-50%.

Whereas Active investing is the opposite, with more fees to pay the fund manager to try and beat the overall market and earn higher returns. Studies completed suggest that picking the right person to entrust your money to is really important, as the majority of active fund managers do not beat the market average over the long run after fees are taken into consideration.

I myself am an active investor, where I have a portfolio of ETF’s, individual stocks and a little bit of crypto. Mainly because I believe based on much research that we will not see a lot of gains in the overall market over the next 10 years, however I still see value in owning companies that have proven to do well over time and will continue to do well in the next 10 years.

Of course, I may be wrong, but for now, you have to decide for yourself what you would rather do.

It is the ultimate Red pill, Blue pill question (if you are a matrix fan), but before you decide, I would suggest speaking to your certified Financial Planner before you start creating your portfolio outside of your super.

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

______________________________________

References:

How to Begin Investing with as Little as $5 Today!

Micro-investing is simply starting with small amounts and continuously adding to your app over time. A great way to start with a small amount, that way you can learn about how you are as an investor.

Wow, we are already halfway through the Beginner Investing Series and I have thoroughly enjoyed writing about some of the things I have learned along the way from my own investing journey.

Of course, this particular series was always meant to be simple and basic, but it was meant to get right to the crux of what I wish I had known before I started investing.

Today though, I will go through how my investing journey began, to give you a great picture of how you to may be able to to start investing with as little as $5.

First of all, my investing journey began after reading “The Barefoot Investor- The only money guide you will ever need.” [1]

Not unlike what you are doing right now, by reading my blog series, I started by just simply seeking to understand how I could make myself more financially savvy and also so I could save up a deposit to buy a house with my wife.

Reading the book, produced a spark that led to me taking action and implementing the steps to help my wife and I to save a deposit for our house, start investing outside of Super and to truly set ourselves up financially.

The spark gathered momentum and I started delving deeper into understanding finance, reading Tony Robbins, “Money: Master the Game” [2] was taking it to another level again. (For a more basic and stream-lined version, check out “Unshakeable.” An amazing read and a must if you want to start investing.)

I can hear you saying, ok but where can I start investing right now, for as little a $5?

Well rest-assured, here it comes…

I want to introduce you to the world of micro-investing!

Yes, if you believe it, you can actually invest your money in an app starting with as little as $5, some may even be as little as $1.

I started my own investing journey using the micro-investing app called Spaceship [4] and I invested using Spaceship up to the point where I felt finally comfortable and knowledgeable enough to take on the markets myself.

Why did I do it and therefore why should you consider it as well?

Time in the market is more important than timing the market

What do I mean by this, I mean that over the long-term, you are more likely to earn a good solid return by having your money in the markets than if you were to try and time it by waiting for everything to dip.

I learned that its better to start investing now and micro-investing apps actually make it possible, rather than waiting to save up $2,000-$5,000 to invest into an ETF, you can start NOW!

2. You can learn by putting some skin in the game!

Learning about your own behaviour whilst having some money in the market was probably the most important aspect I learned and what you can learn with small amounts of money, rather than risking big amounts to start with.

You can learn how you behave when their is a correction in the market (when shares drop by up to 10%, meaning you lose 10% of your money) which is vital to your investing career. Do you pull out because you don’t want to see yourself losing more money? Or do you wait it out until the market goes back up, no matter how long it takes?

Learning this early on has been vital to my own investing success so far. In the last year alone, my own portfolio has grown by 20% and retracted by 10%, but if you do the math, it means it is still up!

3. Finally, it gives you time to research how the market works!

The most important aspect of micro-investing, at least what I got out of it the most, was that I had time to put some money in the market, whilst researching and learning more and more.

You have first-hand experience and you can delve even deeper again by researching into different investment funds, listening to podcasts and learning as much as you can about investing.

If you don’t want to do this, you probably are not cut-out to do active investing, as you need a sound amount of research and knowledge to actively invest.

You may be better off, when you have built up enough money in your micro-investing portfolio, to either seek an advisors guidance or to sink most of your portfolio into ETF’s (exchange traded-funds) that follow a specific index.

I will actually be running through the difference between ETF’s and managed funds in my next blog, as I believe it is really important to understand.

I hope that helped you and if you are interested in micro-investing, it is best to do your research, as Spaceship is not the only app you can start investing with. Another product you could look into is Raiz, but I would highly suggest reading through the PDS and understanding what each investment in the app entails.

At the time of writing, I do not hold any funds in any micro-investing apps.

Until next time,

Take Back Control.

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

_____________________________

References:

[1] - To check out Scott Pape’s book, click the link - https://www.amazon.com.au/Barefoot-Investor-2018-Update-Money/dp/0730324214/ref=asc_df_0730324214/?tag=googleshopdsk-22&linkCode=df0&hvadid=341744699688&hvpos=&hvnetw=g&hvrand=7682030752416799449&hvpone=&hvptwo=&hvqmt=&hvdev=c&hvdvcmdl=&hvlocint=&hvlocphy=9072139&hvtargid=pla-407488791778&psc=1

[2] To check out Tony Robbins, Money: Master the Game, click the link - https://www.catch.com.au/product/money-master-the-game-7-simple-steps-to-financial-freedom-book-by-tony-robbins-796952/?offer_id=37134769&ref=gmc&gclid=Cj0KCQiA15yNBhDTARIsAGnwe0VRyuWdatGHDWjUxavDFYUbByQnFrcymYiK0YJQ-0sLIv240boZhYUaAlxxEALw_wcB

[3] To check out Tony Robbins, Unshakeable, click the link - https://www.amazon.com.au/Unshakeable-Your-Guide-Financial-Freedom/dp/1471164950/ref=asc_df_1471164950/?tag=googleshopdsk-22&linkCode=df0&hvadid=341744699688&hvpos=&hvnetw=g&hvrand=14442430285955173354&hvpone=&hvptwo=&hvqmt=&hvdev=c&hvdvcmdl=&hvlocint=&hvlocphy=9072139&hvtargid=pla-672857091020&psc=1

[4] Spaceship website - https://www.spaceship.com.au/

______________________________

Disclaimer:

General Advice Warning

The information contained in this blog is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser.

Taxation, legal and other matters referred to on this website are of a general nature only and are based on Take Back Control’s interpretation of laws existing at the time and should not be relied upon in place of appropriate professional advice. Those laws may change from time to time.

Where should You Invest your Money?

Where should you invest you money comes down to four simple things that could help you understand exactly where you can invest your money to keep your investing emotions in check.

Once you have decided to start investing, it is really hard to actually decide on where you should invest your money. There is so many different investment vehicles and markets to invest your money that it can get a little overwhelming.

That is why I came up with a simple list (I am a bit of a list maker if you haven’t noticed already) that will help you to start deciding in what investment products/vehicles that could help you achieve your dreams.

Invest in what you know!

Understand your risk tolerance and how you may act if there are any market corrections

Understand that there are multiple investing vehicles out there, such as the bond market, term deposits, REIT’s (Real-estate investment trusts)… It is not all just shares, crypto and cash in the bank.

Consider talking to a trusted advisor who may be able to align your dreams, personal values and financial situation with the investing vehicle that is a right fit for you.

First thing, you need to make sure that you are investing in something that you understand!

The Great Oracle of Omaha, or better known as Warren Buffet, potentially the greatest investor of our time, states that he “Only invests in what he knows and understands… the business has to be simple”

Warren Buffet is a world renowned investor and has an amazing track record of beating the S+P 500 index (An index that tracks the top 500 companies within the USA) over a very long period of time, by doing what he knows best. By buying businesses, because he knows business!

Therefore, what you should do is invest in what you know best too. You should understand what you are investing your money, because if you don’t understand it and your investment decreases in value considerably, you may sell at the wrong time.

In fact, the great Peter Lynch, another long-time investor that I admire said, “You can outperform the experts if you use your edge by investing in companies or industries you already understand.”

Secondly, you should understand your risk tolerance…

One really easy way to do this is by investing a small amount of your hard earned cash in the markets, cash that you don’t need or you are happy to never see again.

I used this simple method of putting money into a micro-investing app (whereby there are no brokerage fees and you can invest as little as $5) to start to understand my own risk tolerance. Sometimes, you just need to have some skin in the game and take a little risk to see what you are like when the markets are going up or coming down.

Thankfully, I was able to see a bit of both, as I had money invested last year in March 2020, whereby the market corrected by a bit over 30%. Meaning I saw my investment and hard-earned money decrease significantly, but I was not phased by it due to my own education, in fact I saw opportunity to buy in even more.

But there were some that did not actually do this, in fact some took money out of their super and sold at the worst possible time.

Which is why understanding risk tolerance is so important to understanding where you will invest your money!

Thirdly, Shares, Crypto and real-estate are not the only investment vehicles out there!

In fact, there is a whole world of financial markets out there…

Ranging from Bonds (whereby you loan money to a bank, government or business and receive interest on that loan essentially) to the Foreign Exchange markets (whereby you can exchange currencies etc.).

You can even buy into Real-estate investment trusts, if you don’t want to buy and hold a physical warehouse or factory, you could buy a portion of it through the REIT.

Which brings me to my final point.

The financial world is a jungle, full of predators, poison ivy and dangerous products/investment vehicles that could leave you disoriented and full of dismay.

That is why having a local guide, such as your trusted Financial Advisor, who is a professional in navigating said financial jungle, can show you how to not only navigate through the jungle. But can show you the plants that you can eat that won’t kill you financially, show you a clear path through so you can reach the other side and also reduce any stress or anxiety you may have about getting lost along the way.

Investing can be scary, it can be exciting and it can truly help you to attain all of your dreams…

And having a trusted advisor who can guide you into the right investment vehicles is worth more than anything you could ever dream of.

If you follow these four simple steps, your investing journey will be smooth-sailing and you will know exactly where to invest your money that is not just right for you, but will help you sleep better at night!

Which is probably the most important thing when it comes to investing and finance.

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

Want Success in Life? Do what 95% of People don’t do…

The top 5% of successful people in the world do two things differently to everyone else.

In a western society where we are so full on with things to do all the time…

Joel Perryman delves into why this is harming the success you want for yourself and goes through on some of the first steps to Taking Back Control of your Life-Health-Wealth

Life gets busy and life seems to be non-stop sometimes, from family and social events to working long hours so you can complete those tasks your boss wanted done yesterday, we all have pretty hectic lives in western society.

In fact, before COVID-19 hit, I remember always responding “I have been crazy busy” to the simple question of, how has your day been?

In fact, if I didn’t respond with how busy I had been, I almost felt like I was letting myself down. I don’t know if this was just me, however in our western society, being busy was a display of success for most people. I felt almost embarrassed to say I didn’t have much on or I had a “chilled” day.

Throughout COVID-19, I became more aware and educated in the ways of Buddhism. Now, I myself am not religious, however I do believe that we can take concepts taught by spiritual leaders such as the Great Buddha and Jesus Christ to challenge us and create a great path for our way of living.

In fact, it was these concepts, as well as the teachings I learned from my literature teachers back in high school who challenged me to think outside the box and to change my perceptions on how I see the world, that led me to become the person I am today.

What does all this have to do with becoming successful, you ask?

Well, all of the above made me STOP and THINK…

It made me STOP to THINK about goals, about life and about what needs to be done to achieve the life you want to live.

To take a deep breath, let life flow by for a little bit and to truly listen to what I want, rather than what others wanted for me.

Once I learned to STOP and THINK, I became more aware of what needed to be done to achieve my own goals, I was able to write out stepping stones towards my dreams and vision of the future.

Just by simply STOPPING and THINKING, you are doing what 95% of people don’t do…

Which is going to help you become more attuned and aligned with your own values and goals, which is one of the first steps to Taking Back Control of your life.

So, do you want success? If so, you need to carve out time to Stop and Think, journal or speak out your thoughts to a recorder. You may be surprised at what ideas and thoughts go through your head, don’t be afraid of them, embrace them.

The success you want in life resides within You and only You, hence why You need to reach inside and pull it out. If there is anything that I have learned over the last ten years talking to people of all backgrounds, it is that a lot of people do not actually know what their own definition of success is.

That is why I want you to Stop and Think about what success means for you?

To help you get started with this, my suggestion would be to;

Create a specific time for you to Stop and Think

Write down ideas in a journal or record it on your mobile

Be curious and let your thoughts flow, best way to do this is be in nature and get rid of all distractions (meaning no social media)

Read it aloud or play it back, I find you truly understand the concepts by doing this

All of the above is a great way to start building on the success you want in life and I believe will help you to Take Back Control,

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

Understand these 3 Investing Secrets before You Invest your first $1…

The 3 Secrets to understand before you start investing is paramount and a must read!

Before you actually begin investing your hard earned money and look at putting your money into businesses and assets, you really need to understand a few things about yourself!

If there is one thing that I have learned from my Financial Planning Degree so far, it is that your emotions get in the way of making sound investing decisions for the future. Behavioural Finance is an interesting topic which delves into the deep recesses of your mind to understand the psychology of people’s spending, investing and saving decisions.

Three well known economists and psychologists laid the frame-work for what is to be known as behavioural finance today; Daniel Kahneman, Amos Tversky and Richard Thaler. All three of these academics wrote papers that has led to our understanding of how investors and even the markets, can make irrational decisions when it comes to managing their portfolio’s. (1)

I won’t delve into Behavioural Finance today, however I will delve into the three cornerstones that should be driving all your investing decisions from here on in. You need to leave emotion (mostly fear of missing out, herd behaviour, greed) at the front door and make every investing decision based on your;

Risk Tolerance

Personal Goals for investing and Time you have to put into it

Personal Values (Environmental Social and Governance)

Understanding these three core things about yourself and why you are investing will help lead your decision making process in all of your investments. Including the investments you make in yourself, such as potentially starting up a business, doing personal development etc.

Firstly, understanding Risk Tolerance is really important.

I am going to use the example of my wife and I, as we have very different risk profiles, where I am seen as very aggressive in my investing and my wife is a little bit more risk averse.

My wife does not like losing money, in fact, she would rather look out for all the savings in the supermarket and is very much of the mind that losing money, no matter the potential upside in the future, is not worth it. She would get anxious and even pull money out of the investments early if she saw a sharp decrease in value.

She would probably rather invest in assets that have a lot less volatility and have consistent income, such as bonds or term deposits.

Whereas I have already ridden waves and corrections previously, in fact, just last year, when we had a 30% decrease in the stock market, I saw the sales stickers that my wife normally sees in the supermarket and decided to buy more, my wife on the other hand would have just seen red.

Therefore, I am more prone to investing in different asset classes than my wife, I also am in what we call the accumulation phase of my life, where I am accumulating wealth. Your risk profile may change as you age, potentially as you stop earning income from a job and retire, you may need to re-assess your own risk profile.

Which comes down to understanding your Personal Goals and the Time you are willing to invest in making your investing decisions.

You truly need to understand why you are investing, I delved deeper into this in one of my Vlogs that you can check out here .

To know your personal goals and why you are investing in the first place will help you to make those key decisions of whether to BUY, SELL or HOLD your investments.

An example is you want to earn capital gains from a company and you find a really great growth company, with revenue increasing by 20% year on year for the last six years. Other than wanting to earn money from that company, what is the reason you would invest in it in the first place?

To save for your future kids education? For an early retirement? So you can see great growth over the next 10 years and then use the capital gains to help create a home deposit?

Investing with an end in mind is super important, which means you need to know your personal goals first. The other thing that goes hand in hand with your goals is understanding how much time you want to be able to put into your investments.

Do you want spend less than an hour per month on your investments? Maybe you have more time and want to spend 1-2 hours per week. Either way, you need to know your goals first and foremost, to then be able to understand how much time you will want to put in.

An example for this is, you may want to set yourself up with no financial worry or stress in the future, that is your goal. Therefore, you won’t want to be watching the markets or spending hours researching for the next up and coming company every week.

Your goals and the lifestyle you wish to live will determine the time you spend on your investments and finances, make sure you understand this along with your risk tolerance and you will know the best assets and investing products to park your money!

** If you are not too dissimilar to the example above, you may want to reach out to a Financial Planner to truly understand your risk profile and personal goals. They can guide you into the right investment vehicles and products for you and your goals!

And finally, understanding your Personal Values is just as important as Risk Tolerance and your Personal Goals.

Do you believe in Free Speech? What about equal rights? Or are you super passionate about climate change?

Would you put your money in a company and support them to grow and become bigger, if you knew they were an arms company?

You need to know where your money is going if you are going to be an investor, because the worst thing that could happen is you start investing in a company or ETF (exchange traded fund) that supports mining or arms manufacturing, but your personal values are against those particular things. Imagine learning that your money helped create guns, or fossil fuels?

These were the two things that my wife specifically said she didn’t want me to invest our money by the way. Therefore, I have only invested our money in companies that I have researched extensively that have nothing to do with mining, the creation of fossil fuels or manufacturing of weapons.

Now, you may have a difference in values and don’t care if you invest in those things or not, however it is best to know what your values are and do your research, or hire an advisor to help you to do so.

So, those are the three secrets you need to understand and know before you start investing, so this and you will be leagues above the average investor, I can assure you!

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

______________________

References:

STOP! Housing Market Going Nuts? And how we could see a decrease in house prices…

Housing prices have increased by 20.3% across Australia on average within 2021!

Within the article, I go through how we ended up here in the first place, where house prices have gone up a crazy amount in a short time. I also go through what may cause the real-estate market to correct significantly within the next 18-24 months!

I wanted to quickly take out some time from our beginners investing series to quickly talk about the housing market and just how bonkers it has been. The scary part, it doesn’t look like housing is going to be going down in price anytime soon!

Not until the government and the central banks take action anyhow, which I will go through what the government will need to do and what action the central bank will take in the next 24-36 months to correct the housing market.

Let me give you a quick understanding of where we are at right now in the housing market…

The Australian median house price has risen by 20.3% in 2021 alone and expected to rise by 25% (1)

People are exacerbating the price increase due to FOMO (Fear of Missing Out) by trying to buy before house prices are out of reach completely.

Buyer demand and sales rates has been super high, due to the FOMO and low supply for houses in the market, which has increased prices considerably. Creating a cut-throat competition right now in the housing market, where buyers are offering anywhere from $30k-$600k above asking price. (depending on suburb of course)

I have been watching in astonishment as weekly numbers come in of sales in Victoria alone, where at the height of lockdown, we were getting anywhere between 83-92% auction clearance rates and private sales of 1,000-1,400 per week. Which, in hindsight from watching these numbers week in-week out over the last few years since buying my first home, has risen substantially. (I remember seeing 600-800 sales on average per week in 2019)

Now we are out of lockdown, sales have increased again to average around 1400-1600 sales per week. (3) Which has left me dumbfounded and I truly believe that people are acting on high amounts of fear and emotion right now.

Of course, this is a great time if you are looking to sell your family home and downgrade because you want to look at retiring, but for anyone looking to buy their first home, it is a little bit deflating to think that your deposit you had been saving the last few years is now not enough for what you want.

How did we actually get here though?

Government policy and the increased incentive to look after home owners to get votes

The Australian real-estate market is valued at a whopping $9 Trillion (up from $7 trillion two years ago), which means the government does not want to see a huge down-turn in prices, as Australians have hedged all their bets and a lot of their wealth into the real-estate market.

The pandemic happened and the central banks (The RBA), fearing a massive downturn, has decreased the cash rate and thus has decreased interest rates to all time lows. Making it easier for companies, businesses and individuals to acquire a loan.

The millennials are growing up and want to move into their very own home, increasing demand!

The expectation and dream of owning your home in Australia is concrete. Most people will not reduce expectation of what they want or where they want to live either, increasing demand in particular suburbs.

The First Home-Buyer and Home-builder policy, which was used to create incentive for first home-buyers and to help with regards to affordability. Unfortunately, the ramifications of this was an increase in buyer demand across the market.

Now that we know how we got here, what is going to happen in the future? Will house prices continue to rise like they have the last 30 years?

I have read a lot of opinions, for that is all they are, no matter whether they come from a real-estate agent or an economist, no one truly knows what will happen. The last twelve months of unprecedented increases in price is case in point for proving everyone wrong.

I cannot tell you whether there will be an increase or decrease over the next year, three years, five or ten. All I can tell you is there are certain things that will need to happen for house prices to cool off.

The Reserve Bank of Australia will need to increase the cash rate, which will in turn increase interest rates on loans. Applying pressure on the amount of loans that will get approved. Problem the RBA has right now in doing this, is that there have been a lot of Australians who have borrowed too much. A sharp increase in rates may reduce the amount of expendable income Australians have for buying things/services, which would impact the overall economy.

The government will need to look at improving supply of houses and create policies to create construction.

The government may need to look at the tax concessions on investment properties, although the last time a government did this, they lost the election.

People may need to reduce their expectations and may need to look at buying elsewhere and not in hot locations. Or potentially look to wait out the strong housing market until they can save up a 20% deposit. Even though prices have been going up consistently, what goes up, must come down, even by a little bit.

I have no idea whether one of these above scenarios will decrease housing prices, or whether all of them need to happen before there is a correction in the real-estate market.

However, I do know that house prices will most likely keep increasing over the next twelve months. The likelihood that they will boom like they have in the last twelve months is low, but we will still see an increase in prices. Albeit, a very small increase, most opinions are between 3-8% over the next twelve months.

With sales at massive highs and supply not meeting the demand, I doubt there will be a correction anytime soon.

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

________________________

References:

When Should You Start Investing?

Starting your investment journey is super exciting, but before you do start that journey, you need to get a few things in order first.

In this article, I write about when is the best time to start investing and when you should start investing.

I always say, the best time to start investing was twenty years ago, the next best time is Now…

But, there is no point starting to invest and start working on accumulating wealth if you have not done the following!

Paid down most commercial debts (ie; car loans, BNPL payments, personal loans, credit card loans)

Grown an emergency fund or save-your-ass fund

Have developed an automated cash flow/budgeting system that means you can sleep at night.

Set-up your Superannuation and review it every 12 months

You could potentially add, buy your first home, to that list if that is a goal of yours in the next three years as well. Essentially, to take a phrase from the well-known Dr. Jordan Peterson, you need to “set your house in order” before you can take on bigger goals, such as investing for the future.

What does, “set your house in order” mean?

Well, it is quite simple, it means that you need to open up the financial closet and clean it out, dust for cobwebs and put your brave pants on to see if there are any nasty creepy crawlies hiding in there.

Which is why you need to complete steps one to four from above, and potentially add step five of buying your first home as well.

Once you have completed all of the above, that is when you can start looking at investing and taking your wealth more seriously. The best part is, you are already investing inside of your super. As long as you are employed, your employer has an obligation to pay you superannuation in Australia, which has tax benefits to you and will be an automated way for you to invest for your future. I would suggest that you check your Super balance and make sure you have been getting these contributions, and if you have not, ask your employer immediately!

(I will not delve into Super in this article today, however I will have a Superannuation series later down the track where I will go through all the Do’s and Don’ts of Super.)

Another reason for setting your house in order and cleaning out your ‘financial closet’ is to make sure that you are not losing sleep at night over money. A survey was complete by the Financial Planning Association of Australia and they found that 20% of men and 27% of women are somewhat stressed about finances.

Which means almost a quarter of those surveyed were most likely losing some sleep at night due to money, which should never be the case, not if you clean out your closet and “set your house in order!”

And finally, the most important reason to not start investing until you have done the above is because you don’t want to lose out on your investments.

Investing to accumulate wealth should be a mid-long term endeavour, meaning you should be holding an investment for seven to ten years. That means, if you have an emergency pop up, you do not want to have to sell that investment, and potentially make a loss, because you didn’t have your house in order.

Investing money in the share market, crypto or any other volatile investment vehicle, that you need today or over the next twelve months, means you increase your risk of losing some or all of that money.

You need to make sure that if you are investing any money, you should be investing money you do not need. I take the mentality that I may even lose all of that money, not that it will happen, just so that I never have to think or worry about having to dip into my investment and potentially lock in losses if something came up.

So, when should you start investing?

When you have been able to set your house in order and cleaned out your financial closet.

Once you have been able to do all of steps one to four and potentially step five, you will be free to use the excess money that you do not need to invest. That is when you could set up a meeting with a professional, such as a Financial Planner, to help you with your investment choices that is specifically tailored to your goals and dreams for the future!

Over the next article, I will be delving into understanding where you could start investing, based off of what risk tolerance you may have and potentially based on your own personal goals, values and the time you want to achieve these.

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

___________________________

References:

What I wish I had learned 10 years ago about Investing!

The one thing I wish I understood more of when I was 18 years old, the one thing I wish someone pulled me aside and showed me the potential there could be from implementing this one thing…

Compound growth and interest is the number one thing you need to learn as an investor!

I cannot accentuate the importance, just read the article where I go through a hypothetical of two people investing in the same vehicle/asset class.

You must understand this before you begin investing, I truly wish I had taken action on this years ago, but better late than never.

Put simply, if you want to know what the number one thing that I have learnt the most since undertaking my studies as a Financial Planner at university is that the best time to invest was 20 years ago, the next best time is TODAY!

A lot of people have used the planting of a tree analogy, where if you want a tree to grow to maturity, the best time to plant it would have been 10, 15 or 20 years ago, the same is for investing. Which is due to one of the most powerful tools you need to have if you want to set yourself up for the future and finally break from financial stress and worry.

The mathematical concept and the greatest wealth creator of all time comes down to one simple concept…

Compound growth and compound interest!

I touched on this a little bit in my earlier article, “What is investing?” However, I want you to truly understand the power of compounding when it comes to investing, because it truly is the game-changer.

Firstly, what is compound growth/interest?

“Compound, to savers and investors, means the ability of a sum of money to grow exponentially over time by the repeated addition of earnings to the principal invested. Each round of earnings adds to the principal that yields the next round of earnings” - Investopedia.com (1)

I daresay, this definition is great, however its best to truly understand compounding by going through a real-life example. I am going to use two people and two different scenarios, one started investing/saving at the age of 18 years old, one started investing 10 years later at the age of 28 years old.

I love graphs, I am a bit of a visual person and it was not until I actually started playing around with some compound interest calculators that I started really understanding what I had missed out on over the past 10 years…

Let’s have a quick look at the two scenarios in the graph below; (2)

Two scenarios of investing, whereby one investor started at age 18 years old, the other started at the age of 28 years. They invested for 32 years and put in $100 regularly every month for 32 years.

Based on the graph above, which is using a pretty conservative 7% annual return over 32 years, (Australian shares on average returned 8.8 per cent annually over 20 years to December 2017) (3) we can see that starting investing 10 years earlier makes a huge difference on the compounding effect.

You can see illustrated in the graph that person 1, who started investing in the share market at 18 years old with an initial deposit of $10,000 and depositing $100 monthly until the age of 45 years old, has been able to accrue $219,414 by the end of the 32 years.

On the other hand, person 2, who started 10 years later, has only been able to accrue $103,111 by the same age of 45 years old.

That is an astounding $116,303 difference…

And here is the rub, the 18 year old person only had to invest $48,400 over the 32 years that they invested, working out to be a measly $1,512 per year. Whereas, person 2, who started at 28 years old, had to invest $36,400, working out to be $1,654 per year over 22 years.

For an extra $12,000 invested from person 1, they were able to get an additional return of $104,303 overall.

I know who I would rather be…

That is just one scenario between two hypothetical people, however imagine if you had started investing when you were 18 years old, I wish I had. However, I started at age 25 years old and I probably lost out on nearly $100,000, but that is ok, I am alright with that, because the teacher does not appear until the student is ready to listen/learn.

I just hope that I can appear in time for you to take action and start investing TODAY, so that you don’t make the mistake of losing out on all those returns that myself and person 2 would have lost.

Going back to the tree analogy, the best time to plant a tree was 20 years ago, but the next best time is right NOW!

So go out and…

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

References -

__________________________

The Number One Secret to Changing Your Life!

The Number one Secret to changing your Life-Health-Wealth and it is one of the most simple things that you can do. I know that over the last two years, whilst we have been in lockdown due to Covid-19, I have been doing a lot more of this one thing.

The foundation to anyone’s success comes back to this, make sure that you read all the way to the end to find out!

I have talked about this already in my first article, whereby I touched on the foundation of Taking Back Control of your Life-Health-Wealth. The foundation is not something I can do for you, it is not something anyone else can do for you either…

You are the only person who can decide and imagine this key and foundational secret to achieving greater Life-Health-Wealth.

It is a skillset in which you can work on and build upon as well, it is forever changing with your ideals, your values and your environment.

The number one secret to changing your life comes down to one thing really, and it seems so simple once you think about it, but so many people don’t do this one thing.

Let me tell you a quick story about two men, or two women, whichever you can identify with the most. One man was outgoing and adventurous when he was younger, he travelled all over the place, going from the party-scenes in Greece, to base camp of Everest. Everyone looked at what he was doing and thought, I would love to do that, it would be amazing to travel and try new things.

Once this man had finally seen most things, he travelled back home, he was late twenties and was now back to a reality he would rather forget. Hemmed down by debt and not knowing what he really wants to do in life, he goes through life, finds a partner, has some kids, buys a house and gets into more debt and works a job he never really liked. He always thinks back to the days where life was easy and care-free and misses those days. He works up until the point he retires, but his health has deteriorated and he is worried about finances because he had never been good at keeping track of his money. He loves his family, but feels empty on the inside.

On the other hand, the other man, or woman, had decided to work and try new things at home. He also wanted to travel and experience life to its fullest, but he was disciplined enough to save up for the times where he travelled. He spoke to career driven people and found his strengths, he dreamed of travelling and helping people. He envisioned a world where his family was happy, care-free and living in the a really nice house. He dreamed of being surrounded by the people his life had touched.

He worked to semi-retire by the age of 45 years old, so he could truly make an impact on his local community, not having to worry about money or stress about trivial things that were not important to him. Fast-forward to his semi-retirement and he feels he is making a difference to other people’s lives, doing what he loves to do day in and day out. He has a family that is supported financially and has everything they ever need and he takes them travelling around the world, without a worry for money or expenses.

Out of the two men, or women, I know who I would rather be…

Of course, everyone is different, but the foundation for achieving a successful Life-Health-Wealth comes down to the one thing that the second wo/man did more than the first. S/He dreamed of the world s/he wanted to be living in within twenty years time, they were able to be disciplined enough to see what they wanted and created goals to achieve it.

It was the idea of imagining this world, this future, being hopeful and believing in themselves to achieve it. DREAMS and envisioning your future is the foundation to achieving anything in life, if you do not have the imagination to dream your life up, I would suggest that you work on it.

Talk with someone who has a dream for their life, their families lives and even for the world. Because if you do not dream and hope for the future, if you just go through life without carving out your own path, you will most likely end up similar to the first man, or woman.

Not sure where to start?

I started by thinking about these two questions, “Where would you like to be in 20 years time, if you had no restrictions, if you were not worried about money or anything, what would a day in the life of You be like? What would you want to be doing 20 years from now?”

I would sit down, with no distractions and start writing if I was you, I have done this many times over, in fact, I do it at the start of every year.

However, if you are not a writer, and would rather talk, record it or even video yourself, do what you can so that you can go back over it and review it. Your dream will change, but if you do not dream and don’t record/write it down somewhere, you will never truly achieve it.

You need the vision to drive you forward, otherwise, you just go through life much like the first man or woman, and you end up just floating through life and before you know it, your life is over.

I want to leave you with those thoughts, thinking and envisioning has got me where I am today, I truly believe it is the foundation to achieving more from your Life-Health-Wealth. It is never too late to start Dreaming!

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

What is Investing?

Investing has been something the wealthy have done for millennia, it is how humanity has been able to progress so quickly over the last 100 years.

With a pooling of resources in order to improve our lives, we have used investing to create wealth, to save lives and even to save the environment.

Read the article to understand what investing really is!

I wanted to start off the blog with something that is trending and quite exciting right now, with major asset classes booming at all time highs, I feel like this would be a great place to begin our journey.

To be honest, even though it is not where I started, I wish it had been, because if I had started investing earlier, I would be a lot wealthier. Of course, with the power of hindsight, we would all change something, so it is best not to dwell on it. That is why I want to start with teaching you a little bit about investing, what it is and just why I wish I had started investing when I was 13 years old!

First of all, the definition of investing is “the act of allocating resources, usually money, with the expectation of generating an income or profit.”- [1]

I like the definition taken from Investopedia, which is a great tool to use if you really want to learn about investing in a lot more detail than what we will be covering in the article today. Now, what does that mean?

Well first of all it is probably best to understand a little bit about Money and also a little bit about the different assets in which you can allocate your money to and why we should do this.

Over the years, I have come up with my own definition of money, which we use as a tool to find a middle-ground between buyers and sellers.

Money is the subjective tool we use to find value in the products and services we wish to attain or buy. It is nothing more than a concept we created to make buying and selling easier, a middle-ground that everyone can accept.

Much like salt, sugar and gold, we used these as mediums of exchange to barter and trade in the past, however it meant that for those that had more knowledge, they could rip more people off. Not to say this doesn’t still happen, but we have a much better system that creates a fair market and opportunity for all.

Thanks to the improvement of this money system, we live in a much more sophisticated and intricate world of economics and globalism, where supply and demand, as well as the overall market, is what sets the prices. I will not bore you with the details here, but just understand, that you as a buyer and seller in the market is needed for prices to be set.

Which is correct for all markets, from food, to real-estate to bonds and shares. Now that you understand, money is nothing more than a tool to make buying and selling easier from person to person, we can delve into the world of investing.

Based on the definition of investing, you need to be able to park your money somewhere, in the hope that the money you invest will make you more money and that newly earned money will also make you more money. (Therefore, $1 becomes $2, that $2 becomes $4 etc.)

That is the beauty of what Albert Einstein called “the 8th Wonder of the World,” yes I am talking about compound interest/earnings.

I won’t get into the details of compounding today, however, compounding is the main reason I would have started investing earlier if I could have.

Now, all this talk of investing is great, but where do you invest your money?

Well, there are plenty of different assets classes to choose from, but today, I will go through the five main asset classes.

Firstly, what is an asset?

“An asset is a resource with economic value that an individual, corporation, or country owns or controls with the expectation that it will provide a future benefit.” [2]

Again, I like the definition from Investopedia, which explains an asset perfectly, it is essentially a resource, like an investment property, a painting, an NFT (non-fungible token), shares in a company/business, etc. That you hold/own in the hope of future economic benefit.

So what are these five main asset classes I was talking about?

Shares/equities

Bonds/coupons

Commodities

Cash

Real-estate

Of course, you could put Crypto in there, but I guess that would fall under commodities, as crypto is very similar to gold, however it could also fall under cash, but we won’t go through that today.

These five different asset classes have been proven to, over the last three hundred years, to make returns consistently. Of course, the asset classes have markets of their own, and these markets go up or down (cycles), but for the majority of the time, they have increased over time.

We can prove this through what we call the S+P/ASX 200, which use to be the Australian All ordinaries index from 1980, before it was replaced with the ASX 200 in 2000. Essentially, the ASX 200 is what we all an index, which is just a group of the top 200 companies in Australia when it comes to their Market capitalisation. Don’t worry too much if you don’t know what this means, just remember that the ASX 200 is a group of the biggest 200 companies in Australia.

Now, if we look all the way back to the year 1938 and the ASX 200 was roughly around 50 basis points, which means you could own 1 unit of the ASX 200 for $50 in 1938. [3]

Now, fast forward to today and the ASX 200 is currently, at the time of writing this article, 7272.7 (bps).

That means $1000 invested in the ASX 200 (Share market) in 1938 would be worth $144,454 today, which does not include dividends paid from investing in the index either.

That sounds pretty sweet, doesn’t it, invest $1000 and make an extra $144,454 on top of your $1,000. That is what investing is about, it is looking to sacrifice in the now, for the hope of future financial returns.

I don’t believe I will have to explain the reason as to why we should be investing, the numbers speak for themselves, but I just wanted you to understand a little bit about investing and the history of it, as I have found this quite helpful in my own investing journey.

I will be going through how to invest, and also what the reason will be to invest in a future article, so please make sure that you subscribe to the blog and our newsletter by clicking the subscribe button.

If you do have any investing questions, or are looking to start your investing journey, I would love to know what your questions are or how you are starting through the comments below;

But until next time,

Take Back Control.

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

_________________________________

References:

[1]- Investopedia- viewed 12/10/21- https://www.investopedia.com/terms/i/investing.asp

[2] Investopedia- viewed 12/10/21- https://www.investopedia.com/terms/a/asset.asp

[3] Market History - viewed 12/10/21 - https://www.marketindex.com.au/history

Let Me Give You the Freedom to Dream!