How to Invest in an Overvalued Market

Have you been thinking of investing in the stock market, or have you already been investing over the last 5-7 years?

The article is a must read for those who are thinking of investing or who have just started investing and want to get a good understanding of how to invest in an overvalued market.

There are multiple strategies, too many to count, and a lot of the portfolio strategies will depend on your current risk tolerance and understanding of the market…

But, there are a few simple things you can do to protect yourself.

Read on to learn about investing in an overvalued market!

The stock market has been on a remarkable run since the pandemic-induced crash in March 2020. The S&P 500 index has more than doubled from its low point, reaching new record highs almost every week. Many investors are wondering if the market is overvalued, and if so, how to invest in such a scenario.

What Does It Mean to Be Overvalued?

A stock or a market is considered overvalued when its current price exceeds its intrinsic value, which is the present value of its future cash flows. There are various methods to estimate the intrinsic value, such as the discounted cash flow analysis, the price-to-earnings ratio, or the asset-based valuation. However, there is no definitive or objective way to measure the intrinsic value, as it depends on many assumptions and estimates.

One popular indicator of market valuation is the Shiller PE ratio, which compares the current price of the S&P 500 index to its average earnings over the past 10 years, adjusted for inflation. The higher the ratio, the more expensive the market is relative to its historical earnings. As of October 2023, the Shiller PE ratio was 38.6, which is well above its long-term average of 16.8 and its median of 15.81. This suggests that the market is overvalued by historical standards.

Why Is the Market Overvalued?

There are many possible reasons why the market is overvalued, such as:

Interest rates: A lot of central banks have increased interest rates over the last two years to combat a higher amount of inflation. Generally, low interest rates make borrowing cheaper, stimulate economic activity, and boost corporate profits. They also make stocks more attractive relative to bonds and other fixed-income investments, as they lower the discount rate used to value future cash flows. However, the opposite is true for higher interest rates, which is why we have seen the market have a massive run on the back of predictions of rate cuts over the short-medium term.

Fiscal stimulus: The U.S. government, and the majority of developed economies, has enacted several fiscal stimulus packages to support the gloably economy during the pandemic, accounting for trillions and trillions of dollars. These stimulus measures have increased consumer spending, business investment, and public infrastructure. They have also increased the money supply and the federal debt, which has lead to inflation and potentially higher taxes in the future, however the central banks seem to think they have done a good enough job currently to stem and even beat inflation.

Earnings recovery: Despite the pandemic, many companies have managed to maintain or increase their earnings, especially in the technology, health care, and consumer sectors. These sectors have benefited from the shift to online services, e-commerce, and digital entertainment. The earnings recovery has boosted investor confidence and optimism about the future growth prospects of these companies.

Emotional trading: Some investors may be driven by emotions, such as fear, greed, or FOMO (fear of missing out), rather than rational analysis. Emotional trading can lead to herd behavior, momentum, and bubbles, which can inflate the market price beyond its fundamental value. Some examples of emotional trading are the GameStop saga, the meme stock craze, and the cryptocurrency frenzy. And now potentially the AI driven bull market that we see before us.

So, How do we Invest in an Overvalued Market?

Investing in an overvalued market can be challenging, as it involves balancing the risk of a market correction or crash with the opportunity of further gains. Some possible strategies are:

Diversify your portfolio: Diversification is a key principle of investing, as it reduces the exposure to any single asset, sector, or market. By diversifying your portfolio across different asset classes, such as stocks, bonds, commodities, real estate, and cash, you can reduce the overall volatility and risk of your portfolio. You can also diversify within each asset class, by investing in different sectors, regions, and styles, such as value, growth, or dividend stocks.

Rebalance your portfolio: Rebalancing is the process of adjusting the weights of your portfolio to match your target asset allocation, which reflects your risk tolerance, time horizon, and goals. Rebalancing can help you maintain your desired level of risk and return, and avoid being overexposed to any asset, sector, or market. Rebalancing can also help you take advantage of market fluctuations, by selling high and buying low, and locking in your gains or losses.

Set stop-loss orders: A stop-loss order is an instruction to sell a security when it reaches a certain price level, which is usually below the current market price. A stop-loss order can help you limit your losses and protect your profits, in case the market drops sharply. However, a stop-loss order can also backfire, if the market rebounds quickly after triggering the order, or if the order is executed at a lower price than the specified level, due to market volatility or liquidity issues.

Consider shorting for experienced investors: Shorting is a strategy that involves selling a security that you do not own, with the expectation of buying it back later at a lower price, and profiting from the price difference. Shorting can be a way to profit from an overvalued market, as it bets on the market decline. However, shorting is also very risky, as it involves borrowing the security, paying interest and fees, and facing unlimited losses if the market rises instead of falls. Shorting is not recommended for novice or long-term investors, as it requires a high level of skill, knowledge, and discipline.

Timing the Market vs. Time in the Market

Some investors may be tempted to time the market, which is the act of moving money in or out of the market based on predictive methods, such as fundamental, technical, or economic analysis. The goal of timing the market is to buy low and sell high, and avoid the market downturns and capture the market upturns. However, timing the market is very difficult, if not impossible, to do consistently and accurately, as it requires predicting the future, which is uncertain and unpredictable.

Many studies have shown that timing the market can be detrimental to long-term returns, as it can cause investors to miss the best days in the market, which often occur during or after the worst days. For example, according to a study by JP Morgan, a $10,000 investment in the S&P 500 between January 1, 2003 and December 30, 2022 would have grown to $64,844 if the investor stayed invested for all days. However, if the investor missed the 10 best days in the market, the investment would have shrunk to $29,7082.

Therefore, instead of timing the market, investors may be better off staying in the market for the long term, and taking advantage of the power of compounding, which is the process of earning returns on returns. By staying in the market, investors can benefit from the long-term upward trend of the market, and smooth out the short-term fluctuations and volatility.

Basically, the stock market may be overvalued by some measures, but that does not mean that it will crash anytime soon. The market can remain overvalued for a long time, or even become more overvalued, as there are many factors that can influence the market price, such as interest rates, fiscal stimulus, earnings recovery, and emotional trading. Investing in an overvalued market can be challenging, but not impossible, if investors follow some strategies, such as diversifying, rebalancing, setting stop-loss orders, and considering shorting for experienced investors. However, the best strategy may be to avoid timing the market, and focus on time in the market, as history has shown that staying invested for the long term can generate competitive returns, regardless of market valuation.

Before looking to jump into the market and begin investing, we would highly suggest to talk to a professional financial adviser or coach that can help you to make the right decision for you and your long term goals.

Until Next Time,

Take Back Control

Risk versus Reward: How to Balance Your Portfolio for Long-Term Success

There is a saying in finance, there is no free lunch, which is true for most things. There is always a payment or trade off for something that you want, no matter what it is.

Investing is no different, you need to understand that investing can be volatile and it pays to know what the historical averages are. However, that does not mean you will have the nerve to hold on to something valuable when it is decreasing in value significantly when the stock market crashes.

Read on about risk v reward how it can lead to investing success, or even failure !

Let me know what you think.

Investing is all about the future, but having a solid understanding of the history of markets can provide clarity and confidence when dealing with uncertainty. One of the most important concepts in investing is the relationship between risk and reward, which measures how much return you can expect for taking on a certain level of risk.

In general, the higher the risk, the higher the potential reward, but also the higher the chance of losing money. Conversely, the lower the risk, the lower the potential reward, but also the lower the chance of losing money. However, risk and reward are not always proportional, and different asset classes can have different risk-reward profiles over time.

Historical Returns by Asset Class

One way to compare the risk and reward of different asset classes is to look at their historical returns over a long period of time. For example, the following table shows the annualized returns and standard deviations of several asset classes from 1985 to 2019. You can check out the Vanguard Asset Class tool to check out data from 1970 through to 2022 here.

Historical Returns by Asset Class - 35 years (1985-2019)

Data for the graph above on 34 years of returns and volatility for each asset class.

As you can see, stocks have historically delivered the highest returns, but also the highest volatility, among the asset classes. Bonds have offered lower returns, but also lower volatility, than stocks. Cash has provided the lowest returns, but also the lowest volatility, among the asset classes. Gold has been a volatile asset class, with returns that have varied significantly over time. REITs have been a relatively high-returning and high-volatility asset class, reflecting the cyclical nature of the real estate market.

However, these historical averages do not tell the whole story. The returns and risks of each asset class can vary significantly from year to year, depending on the economic and market conditions.

There is no clear pattern or ranking of the asset classes over time. Some years, stocks outperform bonds, cash, gold, and REITs, while other years, the opposite is true. Some years, emerging markets lead the pack, while other years, they lag behind. Some years, gold shines as a safe haven, while other years, it loses its lustre. Some years, REITs boom as property prices soar, while other years, they bust as property prices collapse.

How to Manage Risk and Reward in Your Portfolio

So, how can you use this information to balance your portfolio for long-term success? Here are some tips and strategies to consider:

Know your risk tolerance and return objectives over a time horizon. Before you invest, you should have a clear idea of how much risk you are willing and able to take, and how much return you need or want to achieve your financial goals based on a time period. Your risk tolerance and return objectives may depend on factors such as your age, income, expenses, savings, time horizon, and personality. You should also review your risk tolerance and return objectives periodically, as they may change over time.

Diversify across asset classes, sectors, geographies, and styles. One of the most effective ways to reduce your portfolio risk and increase your portfolio reward is to diversify your investments across different asset classes, sectors, geographies, and styles. By doing so, you can reduce the impact of any single asset class, sector, geography, or style on your portfolio performance, and benefit from the different sources of return that each one offers. For example, you can invest in a mix of stocks, bonds, cash, gold, and REITs, as well as in different industries, countries, and market segments, such as value, growth, and quality.

Adopt a long-term perspective and a disciplined approach. Investing is a marathon, not a sprint. You should focus on the long-term performance of your portfolio, rather than the short-term fluctuations of the market. You should also follow a disciplined approach to investing, such as using a buy-and-hold strategy, a dollar-cost averaging strategy, or a rebalancing strategy, to avoid emotional or impulsive decisions that may hurt your portfolio performance. By doing so, you can take advantage of the power of compounding, which can significantly enhance your portfolio returns over time.

Seek professional advice. Investing can be complex and challenging, especially in uncertain and volatile times. You may benefit from seeking professional advice from a qualified financial planner, who can help you design and implement a portfolio that suits your risk tolerance and return objectives, as well as provide ongoing guidance and support.

In summary, risk and reward are two sides of the same coin in investing. You cannot have one without the other. However, you can manage your risk and reward by understanding the historical performance of different asset classes, diversifying your portfolio, adopting a long-term perspective and a disciplined approach, and seeking professional advice. By doing so, you can balance your portfolio for long-term success.

The World is Full of Turbulence Right Now- Creating Opportunities!

Be fearful when others are greedy, and greedy when others are fearful.

“Be fearful when others are greedy and greedy when others are fearful,” a quote from the great value investor, Warren Buffet, the owner of Berkshire Hathaway.

Even if you have not heard of Warren Buffet, even if you have heard of him and you don’t like his methods of investing, you must admit that he has built up some wisdom over the last 57 years since taking over Berkshire Hathaway and building it into the holding company that it is today.

Currently, at time of writing, the ASX 200 (the top 200 listed companies in Australia), is down 13% year to date [1], the S and P 500 (the top 500 companies in the US) is down 25% year to date [2], displaying the fear that we are seeing across the world.

The fear is well-founded, we have no idea what is going to happen next, just look at last week, whereby the British Pound crashed and the central bank had to step in to buy up bonds (bonds are like a loan, being handed out to the government) to save the UK from certain financial catastrophe. [3]Which would have reverberated around the world, even hitting us here in Australia.

Investors are uncertain about what the future entails, and when investors are uncertain, they become fearful, it is known that humans have “loss aversion,” whereby we experience more feelings and emotions from losses than we do from gaining something. [4]

Which generally speaking, losses compound on each other to the point where more people become fearful and will sell down on investments, so that they don’t lose more on their portfolios. Some investors are in need of the cash, therefore they are selling down, due to a myriad of reasons, however most would be selling due to fear of loss right now.

Moving cash from equities/shares to the safe haven of bonds and cash, especially as the cash rate increases.

But, and this is a big but, the companies that people are selling down are still performing, still running their business as usual. The companies are still making money, some are still profiting and handing out dividends, some companies are still pumping into research and development to improve products to become the next Tesla.

All this fear of losses and selling down of assets, it is finally creating opportunities for those willing to do the hard yards and research the companies that are doing well, to understand the companies that are going to do really well in an inflationary environment.

Now, this is not an article to tell you that you should start buying the S and P 500, because it is down 25% this year. No, it is an article just stating the facts, because no one knows just how bad things will get. Or whether the fear is founded on nothing at all and we will see the share market bounce back quickly, as it did in 2020 due to COVID-19 (the bounce back came due to the massive amounts of money that has been pumped into the system, called “quantitative easing”).

However, if you are interested in doing the hard work, and being greedy when others are fearful, you could find some absolutely great companies that are on a fire sale right now.

The worst may not yet have come, we could see further falls in the share markets, but depending on your circumstances and your risk tolerance, there is no reason why you should not be doing your due diligence right now and sifting through the wreckage to salvage some gold.

And just for your knowledge, across time, the share market has always done well, the great companies of the US, Australia, China, Europe, Africa have continued on and forged ahead. Even through wars, famine, droughts and other natural disasters, because nothing can stop human nature. As long as there are still humans on this Earth, there will always be a push for the advancement of the human race, HOPE is what keeps us moving forward.

Hope of course will not see a company or the share market do well, but history shows even after Black Monday, where the Dow Jones crashed by 22.6% in a day, that it will recover. And generally speaking, will do better over the long term, because human progression still keeps marching forward. In the case of Black Monday, half of the losses on that day were made up in just under two days, and it surpassed its previous highs two years later. [5]

Which is why understanding this one fact, that owning a stock is owning part of a company, will help you in these turbulent times. Owning a company or the S and P 500/ASX 200, it is not a gamble if you understand the company and history, if you do your research and hold for the long term, short-term fluctuations will not concern you.

Still, you need to do your due diligence, not just put down money on some company because it has been doing well over the last twelve months, that is when gambling really does come into play.

**If you are unsure of how to value a company and don’t know what to search for in a companies annual statement, that is when talking to a financial advisor could truly help you, or talking to an educated fund manager or investment broker.

I want to leave you on this note, on the 2nd of January, 1950, the S and P 500 opened at 16.660. [2]

Just 72 years later, the S and P 500 is sitting at 3,587, which means you would have $219,309.34 in terms of 1950 dollars if you invested $100. [6]

Not a bad return for just $100. Not to say that historical returns will replicate again, but still, we can learn from history and understand it better, to put ourselves in a position to make better decisions.

Until next time,

Take Back Control

_________________________________________

[1] - Yahoo Finance- search asx 200 (charts)

[2] - Yahoo Finance - search s and p 500 (Charts)

[3] - https://www.barrons.com/articles/bank-of-england-federal-reserve-rate-hikes-51664403126

[4] - https://www.apa.org/science/about/psa/2015/01/gains-losses

[5] - https://www.federalreservehistory.org/essays/stock-market-crash-of-1987

_____________________________________________

Disclaimer:

The information on the Take Back Control Website is intended to be general in nature and is not personal financial product advice. It does not take into account your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. In particular, you should seek independent financial advice and read the relevant product disclosure statement (PDS) or other offer document prior to making an investment decision in relation to a financial product (including a decision about whether to acquire or continue to hold).

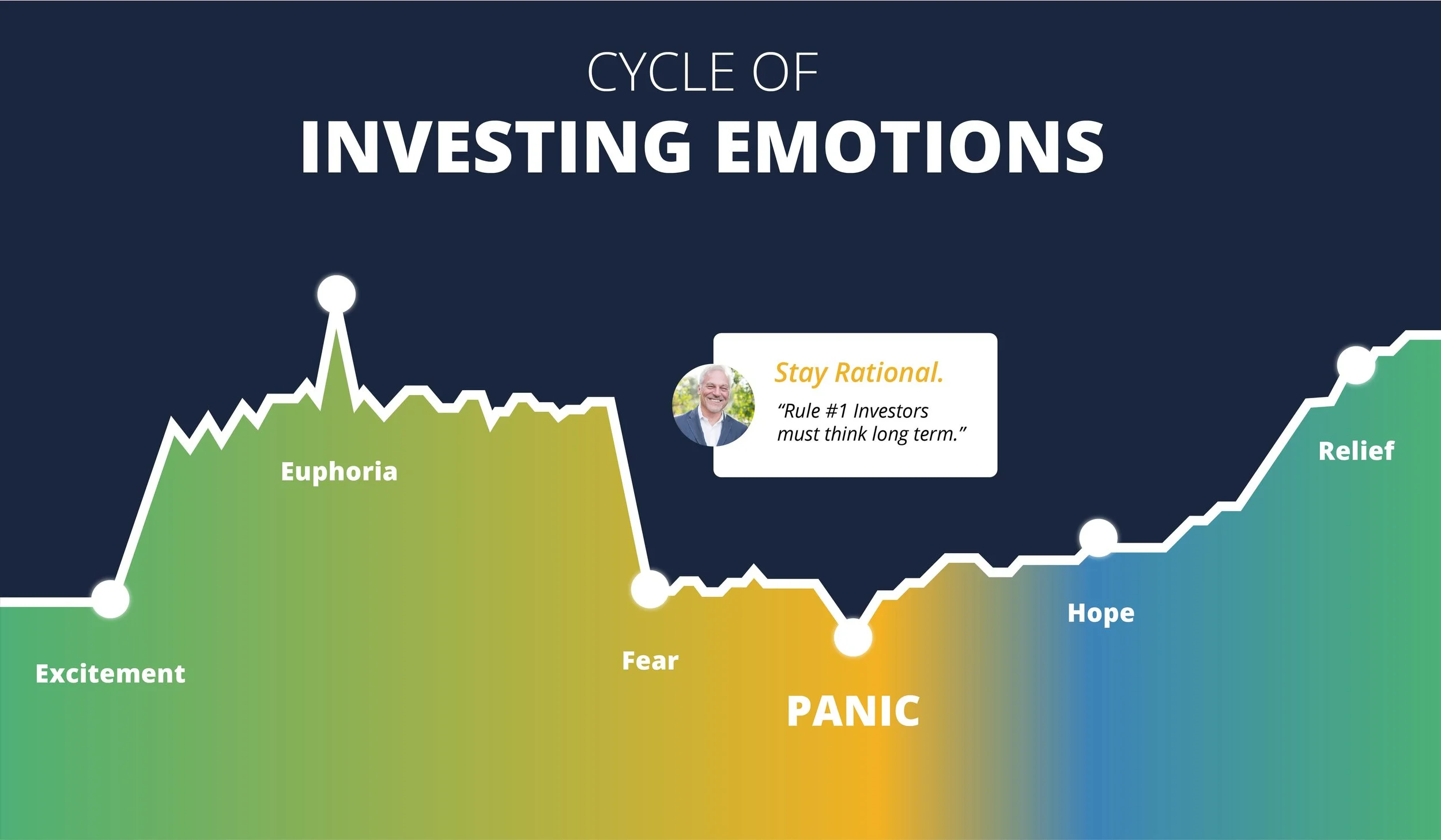

Who else is enjoying the Stock Market Rollercoaster?

The Stock market can be a rollercoaster of a ride, full of uphill thrills, bumps and massive drops!

Only the brave of the brave can handle the ride, are you apart of the brave who is educated enough to stick with it?

Have you felt it yet? The emotional rollercoaster of the stock market, which has literally been going up and down like a yo-yo the last two months, but especially the last month.

The epic highs from last years massive bull run on the stock market left you feeling euphoric, like you could do no wrong.

Which started to slow down by the end of December, and then it picked up right where 2021 left off, hitting what was an all-time record for the ASX 200 (The index tracking the top 200 companies in Australia).

However, by the end of January, we almost saw a correction, where the market dropped significantly by 7-8%, but you would have thought, here is a buying opportunity, “Buy the Dip mentality.”

You would have thought, it will go back up anyhow…

And it did, actually re-gaining 4-5% and then Russia invaded Ukraine, where we saw another dip of 3-4%, driven by major uncertainty in the global economy.

ASX 200- Jan 4th, 2022 - Mar 24, 2022

The ASX 200 is still down nearly 3% from the start of the calendar year. What a ride!!

My portfolio returns for the Month of March

The returns and losses of my very own stock portfolio over the last month has been a hell of a ride, which left me doubting myself at the start of March.

Just looking at the graph’s above, you can see the volatility and it really does look like a rollercoaster track!

Being invested in the market truly has left you feeling like you have been on a ride, full of adrenaline and then the opposite, feeling down right silly and as if you had made a huge mistake.

Over the last month, some investors would have made some massive decisions, whether to buy, sell or hold…

Which given the current climate, the uncertainty in the world, the greater economy and what the future holds, these decisions have been truly difficult.

But, I for one have been enjoying the experience that is the rollercoaster of the stock market the last month. The choices that have needed to be made over the last month was easy for me, as I hope it was for you.

I found myself buying down more shares within the companies that I own in the massive drop in the market at the start of January.

Since Russia has invaded, I have been sitting pretty, where I got myself a bag of popcorn and have just enjoyed the ride.

Were there doubts? Of course there was, especially when my portfolio was showing losses of 15%…

However, what stopped me from selling down and jumping over to the smoother ride that would be the carousel (ie; cash or bonds), was the knowledge of history on the stock market and also knowing the Fundamentals of the businesses I had invested in!!

The stock market, over the course of 200 years, has seen more gains than any other asset!

Knowing this, it is an easy decision, because over the long term, the assets that are held will see returns. The other factor, whereby I know the underlying fundamentals of the business, has left me feeling safe and secure at night.

I have invested in companies that have a huge cash reserve, low debt and are profitable over the last two financial years. Not to mention, their Return on Equity (the return a company has on the equity they use to invest back into the company), has been holding strong at 8-21% over the last ten years.

Meaning, they are very unlikely to go bankrupt, and that management is good enough to ride the waves of war, inflation and much more.

Will some companies be a loss?

Sure, but that will be offset by the gains that other companies will be making over the next 5-20 years!

Which is why I for one have been revelling in the rollercoaster that is the stock market over the last three months.

And I hope you have too.

Ps.

Investing in the stock market is not for everyone and truly depends on your risk tolerance, as well as many other factors regarding your life. If you are thinking about investing in the market, please find a trusted and professional Financial Advisor who can help you navigate the mind-field that is the Financial Markets!

The pure fact of the matter is, it is about learning to control your emotions and figure out who you are as a person.

Until next time,

Take Back Control

Stock Market Corrects-Covid Disrupts Economy

Whilst the stock market may be moving into correction territory, we look to the past to learn more about what may happen within the next year to ten years.

I missed last weeks blog due to exactly what the title says above, Covid doesn’t disrupt the economy, it disrupts lives!

I have been sitting in bed the last three to four days with what has felt like the worst flu of my life, nausea, dizziness, constant headaches, lack of any energy at all and to top it off, my nose just started running…

But we aren’t here to take pity on my plight, if anything we are here to take in the lessons of the last two years. And one thing we have learnt from the last two years is that the economy is set-up by human productivity, and Monetary policy.

So what happens when monetary policy (money-printing from the central banks) will start to ease by potentially as early as the end of next month due to the most recent CPI (Consumer Price Index) report?

**If you are unsure of what the CPI report is and inflation in general, check out this website https://www.investopedia.com/terms/i/inflation.asp

What happens when schools go back and we potentially get an up-tick of Covid cases and therefore more people isolating at home? Therefore decreasing productivity…

I am not one to make predictions or bring out the crystal ball, however I can definitely see how the economy may slow down a little this year, or at the very least within the short-term.

You can see this portrayed through the volatility we have seen in the stock market recently!

All you have to do is check out the last week in the ASX200…

The ASX 200 over the last 5 Trading Days is down 6%

Which is moving into correction territory, which is when we see a drop of 10%.

Source: google.com.au/ASX 200 chart

I am not trying to bring out a fear at all about the market dropping or the economy slowing, but I do want to bring you the facts, just as Covid has disrupted our lives for the last two, nearly three years, there will be more disruptions to come.

You need to know the facts, to make educated decisions and understand that this year may be a tough year for investing.

But there is a silver lining!!

Where there are corrections and down times in the markets, this brings about opportunities for us investors.

I want to teach you the most important lesson as an investor in the equity markets, by simply showing you the graph below;

What you see above is 100 years of data from the All ordinaries index, which later was taken over by the ASX 200 inde. Now as you can see, there are a heap of downturns and corrections in the market, but the main thing I want you to concern yourself with is the starting point of the graph on the y-axis at the very left of the image.

You can roughly see that at the year 1900, the index was priced at about $50, by the end of the century we can see that the markets had increased significantly, even with a heap of downturns and multiple years of catching back up afterwards. The market always ends up better off.

That is why you should not concern yourself with the recent drop in the market, nor the disruptions happening with Covid still running rampant within the community.

If history is anything to go by, we will see the market back in the green and making leaps and bounds, when that will happen, we do not know, but right now, when the market is fearful, it is the best time to invest!

In my next blog, I will be completing the beginning investor series, I look forward to seeing you then,

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

________________________

** The article above only should be used for educational purposes only and is not financial advice, if you wish to invest in the equities market, I highly suggest that you seek advice from a professional that you trust!

The Ultimate Investing question… Passive or Active?

The age old question you need to answer for yourself before you start investing is whether you will be an active investor or passive…

For the majority of you, it will most likely be the latter, but read my blog on the advantages and disadvantages of both.

Investing is really important to growing your wealth and getting to the point where you do not have to work, rather you can choose to work.

Therefore, this is a must read!

Over millennia, we have seen debates around the world about whether you should be an active investor, whereby you have a pretty active role in choosing the assets you buy and sell in your portfolio. Or whether to be a passive investor, whereby you follow the market or a trend you believe will be big in the future.

Over the course of the last few decades, we have seen a pivotal change in the overall consensus of investing, with more people moving into the passive camp.

Today, I want to highlight the advantages and disadvantages of both and to educate you on why I have decided that I shall be an active investor for my own portfolio.

Once you have read through it all, it is up to you to make up your own mind about what style of investor you are going to be.

Passive Investing: “Passive investing is an investment strategy to maximize returns by minimizing buying and selling. Index investing in one common passive investing strategy whereby investors purchase a representative benchmark, such as the S&P 500 index, and hold it over a long time horizon.” - [1]

Advantages:

Diversification, being able spread risk broadly, such as when you invest in the broader market, such as an S&P 500 index.

Lower fees

Tax efficiency

Less time needed for research, simplicity: You do not need to research into every stock or financial product.

Can dollar cost average, instead of timing the market: You can decide to invest a small sum of money every month, three months etc. Rather than trying to time the market, you consistently invest for a set period of time.

Disadvantages:

Subject to total market risk: Whereby if the broader economy is not doing so good, the markets will correct/crash.

You will not see returns higher than the market: As most passive funds, ETF’s etc. They only track the overall market performance.

Seems like a pretty good idea, rather than doing all the work to research the market, just follow the overall market trajectory and returns. You spend less on fees and it is much more tax efficient to put all your money into one index. In fact, for 80-90% of you who are reading this blog right now, it is probably the most effective way to start and continue investing for the long term.

However, with the current market climate and with interest rates on the expected rise, I suspect that active investing will get bigger again over the next few years…

Let’s see why!

Active Investing: “Active investing refers to an investment strategy that involves ongoing buying and selling activity by the investor. Active investors purchase investments and continuously monitor their activity to exploit profitable conditions.” [2]

Advantages:

Flexibility: Active managers aren't required to follow a specific index. They can buy those "diamond in the rough" stocks they believe they've found.

Hedging: Active managers can also hedge their bets using various techniques such as short sales or put options, and they're able to exit specific stocks or sectors when the risks become too big. Passive managers are stuck with the stocks that the index they track holds, regardless of how they are doing.

Tax management: Even though this strategy could trigger a capital gains tax, advisors can tailor tax management strategies to individual investors, such as by selling investments that are losing money to offset the taxes on the big winners.

Risk management: Active investors and fund managers can select stocks based on the prevailing market conditions.

Short-term opportunities: Active investors can make use of short term (3 months or less) opportunities, which in turn gives them a range of tools to choose from when investing.

Have more opportunities to invest in different asset classes: Active investors and funds are more likely to be able to delve into different asset classes, therefore diversifying risk away again.

Can meet specific needs of ethical and moral criteria: With most passive funds, a lot of them do not meet a lot of investors criteria, such as not to invest in mining, or child slavery. When you invest in the top 500 companies in the U.S for example, you have no idea what these companies are doing with your money.

Disadvantages:

Very expensive: The average expense ratio is 1.4 percent for an actively managed equity fund, compared to only 0.6 percent for the average passive equity fund. Fees are higher because all that active buying and selling triggers transaction costs.. All those fees over decades of investing can kill returns.

Active risk: Active managers are free to buy any investment they think would bring high returns, which is great when the analysts are right but terrible when they're wrong.

Poor track record: The data show that very few actively managed portfolios beat their passive benchmarks, especially after taxes and fees are accounted for. Indeed, over medium to long time frames, only a small handful of actively managed mutual funds surpass their benchmark index.

Minimum Investment amounts: Some Actively managed funds in fact need a minimum to invest in that fund, such as $10,000. Or some brokerage platforms need a minimum of $100 per trade etc.

As you can see, the age old question of Active versus passive comes down to a few things, whether you have the time to do the research, whether you are ok taking on more risk for more specific investments, and also whether you can take on some more complexity regarding tax etc.

At the end of it all, it mostly comes down to whether you also believe the wider market will do well over the long term or whether you have the confidence and knowledge to beat the markets over the long term.

Majority of the time, you won’t beat the market, so it is truly up to you to decide whether you are a passive or active investor.

I have decided that I want to follow along the path of active investing, to test my own knowledge and because I believe that the overall markets will not increase significantly over the next ten years. I do not see a lot of growth to be had, however I may be entirely wrong and therefore you need to make your own decision on what you should do as an investor.

Let me know in the comments below what path you will choose,

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

_______________________________________

References List:

[1] - https://www.investopedia.com/terms/p/passiveinvesting.asp

[2] - https://www.investopedia.com/terms/a/activeinvesting.asp

Where should You Invest your Money?

Where should you invest you money comes down to four simple things that could help you understand exactly where you can invest your money to keep your investing emotions in check.

Once you have decided to start investing, it is really hard to actually decide on where you should invest your money. There is so many different investment vehicles and markets to invest your money that it can get a little overwhelming.

That is why I came up with a simple list (I am a bit of a list maker if you haven’t noticed already) that will help you to start deciding in what investment products/vehicles that could help you achieve your dreams.

Invest in what you know!

Understand your risk tolerance and how you may act if there are any market corrections

Understand that there are multiple investing vehicles out there, such as the bond market, term deposits, REIT’s (Real-estate investment trusts)… It is not all just shares, crypto and cash in the bank.

Consider talking to a trusted advisor who may be able to align your dreams, personal values and financial situation with the investing vehicle that is a right fit for you.

First thing, you need to make sure that you are investing in something that you understand!

The Great Oracle of Omaha, or better known as Warren Buffet, potentially the greatest investor of our time, states that he “Only invests in what he knows and understands… the business has to be simple”

Warren Buffet is a world renowned investor and has an amazing track record of beating the S+P 500 index (An index that tracks the top 500 companies within the USA) over a very long period of time, by doing what he knows best. By buying businesses, because he knows business!

Therefore, what you should do is invest in what you know best too. You should understand what you are investing your money, because if you don’t understand it and your investment decreases in value considerably, you may sell at the wrong time.

In fact, the great Peter Lynch, another long-time investor that I admire said, “You can outperform the experts if you use your edge by investing in companies or industries you already understand.”

Secondly, you should understand your risk tolerance…

One really easy way to do this is by investing a small amount of your hard earned cash in the markets, cash that you don’t need or you are happy to never see again.

I used this simple method of putting money into a micro-investing app (whereby there are no brokerage fees and you can invest as little as $5) to start to understand my own risk tolerance. Sometimes, you just need to have some skin in the game and take a little risk to see what you are like when the markets are going up or coming down.

Thankfully, I was able to see a bit of both, as I had money invested last year in March 2020, whereby the market corrected by a bit over 30%. Meaning I saw my investment and hard-earned money decrease significantly, but I was not phased by it due to my own education, in fact I saw opportunity to buy in even more.

But there were some that did not actually do this, in fact some took money out of their super and sold at the worst possible time.

Which is why understanding risk tolerance is so important to understanding where you will invest your money!

Thirdly, Shares, Crypto and real-estate are not the only investment vehicles out there!

In fact, there is a whole world of financial markets out there…

Ranging from Bonds (whereby you loan money to a bank, government or business and receive interest on that loan essentially) to the Foreign Exchange markets (whereby you can exchange currencies etc.).

You can even buy into Real-estate investment trusts, if you don’t want to buy and hold a physical warehouse or factory, you could buy a portion of it through the REIT.

Which brings me to my final point.

The financial world is a jungle, full of predators, poison ivy and dangerous products/investment vehicles that could leave you disoriented and full of dismay.

That is why having a local guide, such as your trusted Financial Advisor, who is a professional in navigating said financial jungle, can show you how to not only navigate through the jungle. But can show you the plants that you can eat that won’t kill you financially, show you a clear path through so you can reach the other side and also reduce any stress or anxiety you may have about getting lost along the way.

Investing can be scary, it can be exciting and it can truly help you to attain all of your dreams…

And having a trusted advisor who can guide you into the right investment vehicles is worth more than anything you could ever dream of.

If you follow these four simple steps, your investing journey will be smooth-sailing and you will know exactly where to invest your money that is not just right for you, but will help you sleep better at night!

Which is probably the most important thing when it comes to investing and finance.

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

When Should You Start Investing?

Starting your investment journey is super exciting, but before you do start that journey, you need to get a few things in order first.

In this article, I write about when is the best time to start investing and when you should start investing.

I always say, the best time to start investing was twenty years ago, the next best time is Now…

But, there is no point starting to invest and start working on accumulating wealth if you have not done the following!

Paid down most commercial debts (ie; car loans, BNPL payments, personal loans, credit card loans)

Grown an emergency fund or save-your-ass fund

Have developed an automated cash flow/budgeting system that means you can sleep at night.

Set-up your Superannuation and review it every 12 months

You could potentially add, buy your first home, to that list if that is a goal of yours in the next three years as well. Essentially, to take a phrase from the well-known Dr. Jordan Peterson, you need to “set your house in order” before you can take on bigger goals, such as investing for the future.

What does, “set your house in order” mean?

Well, it is quite simple, it means that you need to open up the financial closet and clean it out, dust for cobwebs and put your brave pants on to see if there are any nasty creepy crawlies hiding in there.

Which is why you need to complete steps one to four from above, and potentially add step five of buying your first home as well.

Once you have completed all of the above, that is when you can start looking at investing and taking your wealth more seriously. The best part is, you are already investing inside of your super. As long as you are employed, your employer has an obligation to pay you superannuation in Australia, which has tax benefits to you and will be an automated way for you to invest for your future. I would suggest that you check your Super balance and make sure you have been getting these contributions, and if you have not, ask your employer immediately!

(I will not delve into Super in this article today, however I will have a Superannuation series later down the track where I will go through all the Do’s and Don’ts of Super.)

Another reason for setting your house in order and cleaning out your ‘financial closet’ is to make sure that you are not losing sleep at night over money. A survey was complete by the Financial Planning Association of Australia and they found that 20% of men and 27% of women are somewhat stressed about finances.

Which means almost a quarter of those surveyed were most likely losing some sleep at night due to money, which should never be the case, not if you clean out your closet and “set your house in order!”

And finally, the most important reason to not start investing until you have done the above is because you don’t want to lose out on your investments.

Investing to accumulate wealth should be a mid-long term endeavour, meaning you should be holding an investment for seven to ten years. That means, if you have an emergency pop up, you do not want to have to sell that investment, and potentially make a loss, because you didn’t have your house in order.

Investing money in the share market, crypto or any other volatile investment vehicle, that you need today or over the next twelve months, means you increase your risk of losing some or all of that money.

You need to make sure that if you are investing any money, you should be investing money you do not need. I take the mentality that I may even lose all of that money, not that it will happen, just so that I never have to think or worry about having to dip into my investment and potentially lock in losses if something came up.

So, when should you start investing?

When you have been able to set your house in order and cleaned out your financial closet.

Once you have been able to do all of steps one to four and potentially step five, you will be free to use the excess money that you do not need to invest. That is when you could set up a meeting with a professional, such as a Financial Planner, to help you with your investment choices that is specifically tailored to your goals and dreams for the future!

Over the next article, I will be delving into understanding where you could start investing, based off of what risk tolerance you may have and potentially based on your own personal goals, values and the time you want to achieve these.

Until next time,

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

___________________________

References:

What I wish I had learned 10 years ago about Investing!

The one thing I wish I understood more of when I was 18 years old, the one thing I wish someone pulled me aside and showed me the potential there could be from implementing this one thing…

Compound growth and interest is the number one thing you need to learn as an investor!

I cannot accentuate the importance, just read the article where I go through a hypothetical of two people investing in the same vehicle/asset class.

You must understand this before you begin investing, I truly wish I had taken action on this years ago, but better late than never.

Put simply, if you want to know what the number one thing that I have learnt the most since undertaking my studies as a Financial Planner at university is that the best time to invest was 20 years ago, the next best time is TODAY!

A lot of people have used the planting of a tree analogy, where if you want a tree to grow to maturity, the best time to plant it would have been 10, 15 or 20 years ago, the same is for investing. Which is due to one of the most powerful tools you need to have if you want to set yourself up for the future and finally break from financial stress and worry.

The mathematical concept and the greatest wealth creator of all time comes down to one simple concept…

Compound growth and compound interest!

I touched on this a little bit in my earlier article, “What is investing?” However, I want you to truly understand the power of compounding when it comes to investing, because it truly is the game-changer.

Firstly, what is compound growth/interest?

“Compound, to savers and investors, means the ability of a sum of money to grow exponentially over time by the repeated addition of earnings to the principal invested. Each round of earnings adds to the principal that yields the next round of earnings” - Investopedia.com (1)

I daresay, this definition is great, however its best to truly understand compounding by going through a real-life example. I am going to use two people and two different scenarios, one started investing/saving at the age of 18 years old, one started investing 10 years later at the age of 28 years old.

I love graphs, I am a bit of a visual person and it was not until I actually started playing around with some compound interest calculators that I started really understanding what I had missed out on over the past 10 years…

Let’s have a quick look at the two scenarios in the graph below; (2)

Two scenarios of investing, whereby one investor started at age 18 years old, the other started at the age of 28 years. They invested for 32 years and put in $100 regularly every month for 32 years.

Based on the graph above, which is using a pretty conservative 7% annual return over 32 years, (Australian shares on average returned 8.8 per cent annually over 20 years to December 2017) (3) we can see that starting investing 10 years earlier makes a huge difference on the compounding effect.

You can see illustrated in the graph that person 1, who started investing in the share market at 18 years old with an initial deposit of $10,000 and depositing $100 monthly until the age of 45 years old, has been able to accrue $219,414 by the end of the 32 years.

On the other hand, person 2, who started 10 years later, has only been able to accrue $103,111 by the same age of 45 years old.

That is an astounding $116,303 difference…

And here is the rub, the 18 year old person only had to invest $48,400 over the 32 years that they invested, working out to be a measly $1,512 per year. Whereas, person 2, who started at 28 years old, had to invest $36,400, working out to be $1,654 per year over 22 years.

For an extra $12,000 invested from person 1, they were able to get an additional return of $104,303 overall.

I know who I would rather be…

That is just one scenario between two hypothetical people, however imagine if you had started investing when you were 18 years old, I wish I had. However, I started at age 25 years old and I probably lost out on nearly $100,000, but that is ok, I am alright with that, because the teacher does not appear until the student is ready to listen/learn.

I just hope that I can appear in time for you to take action and start investing TODAY, so that you don’t make the mistake of losing out on all those returns that myself and person 2 would have lost.

Going back to the tree analogy, the best time to plant a tree was 20 years ago, but the next best time is right NOW!

So go out and…

Take Back Control

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

References -

__________________________

What is Investing?

Investing has been something the wealthy have done for millennia, it is how humanity has been able to progress so quickly over the last 100 years.

With a pooling of resources in order to improve our lives, we have used investing to create wealth, to save lives and even to save the environment.

Read the article to understand what investing really is!

I wanted to start off the blog with something that is trending and quite exciting right now, with major asset classes booming at all time highs, I feel like this would be a great place to begin our journey.

To be honest, even though it is not where I started, I wish it had been, because if I had started investing earlier, I would be a lot wealthier. Of course, with the power of hindsight, we would all change something, so it is best not to dwell on it. That is why I want to start with teaching you a little bit about investing, what it is and just why I wish I had started investing when I was 13 years old!

First of all, the definition of investing is “the act of allocating resources, usually money, with the expectation of generating an income or profit.”- [1]

I like the definition taken from Investopedia, which is a great tool to use if you really want to learn about investing in a lot more detail than what we will be covering in the article today. Now, what does that mean?

Well first of all it is probably best to understand a little bit about Money and also a little bit about the different assets in which you can allocate your money to and why we should do this.

Over the years, I have come up with my own definition of money, which we use as a tool to find a middle-ground between buyers and sellers.

Money is the subjective tool we use to find value in the products and services we wish to attain or buy. It is nothing more than a concept we created to make buying and selling easier, a middle-ground that everyone can accept.

Much like salt, sugar and gold, we used these as mediums of exchange to barter and trade in the past, however it meant that for those that had more knowledge, they could rip more people off. Not to say this doesn’t still happen, but we have a much better system that creates a fair market and opportunity for all.

Thanks to the improvement of this money system, we live in a much more sophisticated and intricate world of economics and globalism, where supply and demand, as well as the overall market, is what sets the prices. I will not bore you with the details here, but just understand, that you as a buyer and seller in the market is needed for prices to be set.

Which is correct for all markets, from food, to real-estate to bonds and shares. Now that you understand, money is nothing more than a tool to make buying and selling easier from person to person, we can delve into the world of investing.

Based on the definition of investing, you need to be able to park your money somewhere, in the hope that the money you invest will make you more money and that newly earned money will also make you more money. (Therefore, $1 becomes $2, that $2 becomes $4 etc.)

That is the beauty of what Albert Einstein called “the 8th Wonder of the World,” yes I am talking about compound interest/earnings.

I won’t get into the details of compounding today, however, compounding is the main reason I would have started investing earlier if I could have.

Now, all this talk of investing is great, but where do you invest your money?

Well, there are plenty of different assets classes to choose from, but today, I will go through the five main asset classes.

Firstly, what is an asset?

“An asset is a resource with economic value that an individual, corporation, or country owns or controls with the expectation that it will provide a future benefit.” [2]

Again, I like the definition from Investopedia, which explains an asset perfectly, it is essentially a resource, like an investment property, a painting, an NFT (non-fungible token), shares in a company/business, etc. That you hold/own in the hope of future economic benefit.

So what are these five main asset classes I was talking about?

Shares/equities

Bonds/coupons

Commodities

Cash

Real-estate

Of course, you could put Crypto in there, but I guess that would fall under commodities, as crypto is very similar to gold, however it could also fall under cash, but we won’t go through that today.

These five different asset classes have been proven to, over the last three hundred years, to make returns consistently. Of course, the asset classes have markets of their own, and these markets go up or down (cycles), but for the majority of the time, they have increased over time.

We can prove this through what we call the S+P/ASX 200, which use to be the Australian All ordinaries index from 1980, before it was replaced with the ASX 200 in 2000. Essentially, the ASX 200 is what we all an index, which is just a group of the top 200 companies in Australia when it comes to their Market capitalisation. Don’t worry too much if you don’t know what this means, just remember that the ASX 200 is a group of the biggest 200 companies in Australia.

Now, if we look all the way back to the year 1938 and the ASX 200 was roughly around 50 basis points, which means you could own 1 unit of the ASX 200 for $50 in 1938. [3]

Now, fast forward to today and the ASX 200 is currently, at the time of writing this article, 7272.7 (bps).

That means $1000 invested in the ASX 200 (Share market) in 1938 would be worth $144,454 today, which does not include dividends paid from investing in the index either.

That sounds pretty sweet, doesn’t it, invest $1000 and make an extra $144,454 on top of your $1,000. That is what investing is about, it is looking to sacrifice in the now, for the hope of future financial returns.

I don’t believe I will have to explain the reason as to why we should be investing, the numbers speak for themselves, but I just wanted you to understand a little bit about investing and the history of it, as I have found this quite helpful in my own investing journey.

I will be going through how to invest, and also what the reason will be to invest in a future article, so please make sure that you subscribe to the blog and our newsletter by clicking the subscribe button.

If you do have any investing questions, or are looking to start your investing journey, I would love to know what your questions are or how you are starting through the comments below;

But until next time,

Take Back Control.

If you have found this Blog valuable, I would love it if you shared it with friends and family. The more the merrier, as I want to see each and every one of you learn to Take Back Control of your Life-Health-Wealth !

_________________________________

References:

[1]- Investopedia- viewed 12/10/21- https://www.investopedia.com/terms/i/investing.asp

[2] Investopedia- viewed 12/10/21- https://www.investopedia.com/terms/a/asset.asp

[3] Market History - viewed 12/10/21 - https://www.marketindex.com.au/history